Family with two teenagers meeting with attorney at office desk to discuss wrongful death settlement documents

Structured Settlement Wrongful Death Guide for Families

Content

The death of a loved one through negligence creates a dual crisis. Grief compounds financial pressure. You're navigating funeral arrangements while wondering how to replace lost income, pay the mortgage, fund college tuition for children who've already lost so much.

When wrongful death litigation produces a settlement or verdict, families face a choice with permanent consequences: take the money now as a single check, or arrange structured payments spreading over years or decades. This isn't merely a financial calculation—it shapes whether your 16-year-old has college funds at 18, whether your surviving parent receives reliable income at 75, whether the entire recovery evaporates within two years because relatives pressured someone into "lending" money for failing business ventures.

Annuity settlement options designed specifically for wrongful death claims convert catastrophic loss into durable financial protection. But they work only if structured correctly before settlement documents get signed.

What Makes Wrongful Death Settlements Different from Other Injury Claims

Personal injury money belongs to the injured person. Simple. Wrongful death compensation flows to survivors—plural—creating complexity.

State statutes determine who counts as a beneficiary. Most prioritize spouses and children. Some include parents if no spouse or children survive. California might divide proceeds equally among a surviving spouse and three adult children. Florida's distribution formula changes based on whether minor children are involved versus only adults. Texas has its own rules. Georgia yet another set.

Multiple beneficiaries create competing needs. Consider a widow at 45 who needs income replacement for four decades or more. Her 19-year-old needs education costs now, maybe a home down payment in five years. The 12-year-old daughter needs protection until she develops financial maturity—sometime well past 18 for most people, despite what the law says about adulthood.

Give each person their share as cash? Each must separately invest and manage their portion. Four separate opportunities for mismanagement. The son might blow through his share by 23. The daughter faces pressure from a manipulative romantic partner at 20. The widow falls victim to a financial advisor churning her account for commissions.

Structured settlements solve this by creating customized payment streams. The widow gets monthly lifetime income. The college-aged son receives quarterly payments for four academic years, then $150,000 when he turns 24. The minor daughter's portion stays protected in structured annuities until 25, with education disbursements built in during college years. One coordinated strategy prevents the common disaster where some family members drain their shares quickly while others conserve—breeding resentment when the spenders return asking for loans.

The goal of any settlement structure should not be to maximize a number on paper, but to build a financial architecture that protects the family through every season of life — from the rawness of early grief to the quiet vulnerabilities of old age. Money without structure is just opportunity for loss

— Richard B. Risk

State laws add wrinkles. Some jurisdictions require court approval when minors receive settlements, with judges scrutinizing whether the proposed structure adequately protects children. Texas courts frequently mandate structured settlements for minors rather than allowing lump sums. Other states permit more flexibility.

Estate and inheritance taxes vary by state too. Nine states impose estate taxes with thresholds as low as $1 million in Oregon. How you structure wrongful death proceeds affects whether the settlement pushes an estate over exemption thresholds, potentially costing beneficiaries hundreds of thousands in unnecessary taxes.

Author: Michael Thornton;

Source: mannawong.com

How Structured Settlements Work in Wrongful Death Cases

Who Receives Payments and How They're Distributed

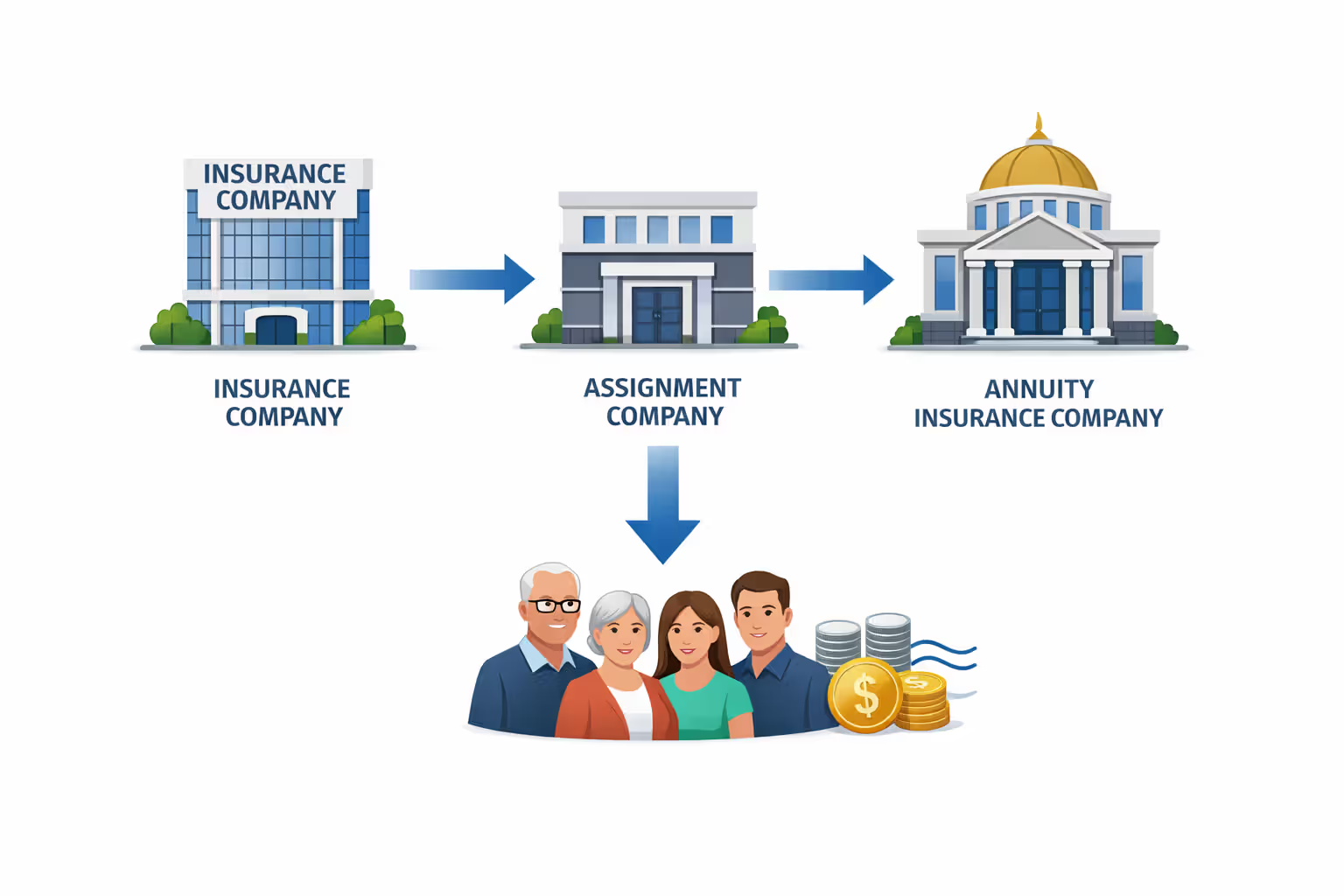

Settlement agreements name each beneficiary and specify their payment terms. The defendant's insurance company doesn't send checks every month for decades—that would create risk if the insurer encountered financial trouble years later.

Instead, the insurer purchases qualified assignment annuities from highly-rated life insurance companies. These annuities become irrevocable obligations to make scheduled payments regardless of what happens to the defendant or their insurer.

Assignment companies serve as intermediaries. They assume the defendant's payment obligation and purchase the annuity. This legal structure—authorized under IRC Section 130—lets the assignment company fund the annuity with pre-tax dollars while beneficiaries receive tax-free payments. The assignment company profits from the spread between what the annuity costs and the settlement amount.

Each beneficiary owns their annuity independently. A mother receiving payments for her deceased son owns hers separately from co-beneficiaries. If she dies before exhausting her payment stream, remaining guaranteed payments typically flow to her estate or to contingent beneficiaries she designated, depending on how the annuity was structured. This differs from joint-and-survivor arrangements where payments might continue to a secondary person at full or reduced amounts.

The Role of Annuities in Creating Payment Streams

Qualified structured settlement annuities differ from retail annuities sold to individual investors. They're institutional products unavailable on the open market, frequently offering better rates because they're purchased in large blocks.

The issuing life insurance company invests the premium in its general account—primarily investment-grade bonds and similar fixed-income securities—and guarantees payment performance regardless of actual investment returns.

These guaranteed payment lawsuit settlements eliminate investment risk entirely. Stock market crashes or soars? Payments arrive on schedule either way. For families who've never managed six or seven figures, this guarantee prevents the devastating losses that plague injury victims who take lump sums. The National Structured Settlements Trade Association found one-third of injury victims taking lump sums exhaust the money within five years.

Annuity settlement options include period-certain structures—payments for exactly 10, 20, or 30 years. Also lifetime payments continuing until death. Or hybrid approaches combining both.

Period-certain annuities guarantee total payout even if the beneficiary dies early. Remaining payments go to their estate. Lifetime annuities provide longevity protection, continuing regardless of how long someone lives, though payments stop at death unless structured with minimum guarantee periods.

Rating agencies assess annuity issuers' financial strength. Settlements typically require carriers rated A+ or better by A.M. Best, or equivalent from Moody's or Standard & Poor's. Some settlements split annuity purchases across multiple carriers to stay within state guaranty association coverage limits—usually $250,000 per person per company, though limits vary. These guaranty associations protect annuity owners if an insurance company fails.

Author: Michael Thornton;

Source: mannawong.com

Comparing Lump Sum vs. Structured Payments for Wrongful Death Compensation

Immediate full payment versus scheduled distributions? Each path involves specific advantages and drawbacks:

| Decision Factor | Taking Everything Now | Scheduled Payments Over Time |

| Tax Implications | Settlement principal escapes taxes; earnings on invested funds face ordinary income or capital gains taxes annually | Every payment arrives completely tax-free forever including all accumulated growth |

| Who Bears Risk | Family assumes all market volatility and investment management responsibility | Insurance carrier absorbs risk; payments arrive as contracted regardless of market conditions |

| Creditor Threats | Exposed to lawsuits, judgment liens, creditor claims, and bankruptcy proceedings | Robust statutory protections in most jurisdictions; future payment rights typically exempt from collection |

| Access to Funds | Unrestricted control; withdraw or spend any amount whenever desired | Minimal flexibility; modifying payment terms after signing essentially impossible without selling payment rights at steep discounts |

| Income Certainty | Zero guarantees; outcome depends entirely on investment decisions and market performance | Contractually locked regardless of economic conditions, market crashes, or personal circumstances |

| Keeping Pace with Inflation | Achievable through growth investments; success not guaranteed | Cost-of-living increases available but reduce initial payment amounts |

| Management Burden | Demands active oversight or paying advisor fees annually | Zero management decisions required; payments arrive automatically |

| Ideal Candidates | Financially sophisticated individuals comfortable with investment risk; families facing immediate major expenses like medical debts | Anyone needing reliable long-term income; protection from mismanagement; beneficiaries lacking investment experience |

Structured settlement benefits show most dramatically for beneficiaries at high risk of mismanagement. Minors receiving funds at 18 rarely possess the judgment to handle substantial money. Individuals struggling with addiction face unique vulnerabilities. Those with cognitive disabilities affecting financial judgment. Family members who've never handled more than a few thousand dollars suddenly controlling hundreds of thousands or millions.

A $2 million settlement structured over 30 years might deliver $3.5 million total because of tax-free compounding, whereas the same lump sum invested in taxable accounts requires sustained 6-7% after-tax returns just to match that outcome—a challenging benchmark.

Long term payout plans also shield against predatory relatives, romance scammers, and terrible decisions made while grieving. That first year after losing someone? Judgment suffers. Major financial choices during acute grief frequently produce lasting regret. Structured payments prevent irreversible mistakes while emotions run high.

Lump sums suit specific circumstances better though. Families facing imminent foreclosure need funds immediately. Beneficiaries with terminal illnesses benefit more from present access than future payments decades away. Sophisticated investors with proven track records might generate returns exceeding annuity rates, particularly when interest rates are rising and annuity pricing becomes less attractive.

Tax Treatment: Why Wrongful Death Structured Settlements Offer Unique Advantages

Internal Revenue Code Section 104(a)(2) excludes from gross income damages received for personal physical injuries or physical sickness, whether through lawsuit or settlement. This exclusion extends to wrongful death since it compensates for the deceased's physical injuries causing death.

Tax advantages settlements provide extend beyond just the initial principal escaping taxation.

With lump sums, the settlement amount itself remains tax-free initially. But interest, dividends, or capital gains generated by investing those funds? All taxable at ordinary income rates or capital gains rates. Take $1 million, invest in bonds yielding 4%. That generates $40,000 in annual taxable income. Over 25 years, taxes on investment returns could consume $200,000-$300,000 depending on the beneficiary's tax bracket.

Structured settlements bypass this tax drag completely. The annuity grows tax-deferred inside the insurance company's investment portfolio. Payments to beneficiaries remain entirely tax-free. A $1 million settlement structured to deliver $55,000 annually for 30 years pays $1.65 million total—all tax-free. Achieving equivalent after-tax returns in taxable accounts requires significantly higher gross returns.

Estate tax considerations add another dimension. For wealthier families, a large lump sum added to the estate might push total assets above federal estate tax exemption levels ($12.92 million per individual in 2023, scheduled to drop to roughly $6 million in 2026). Nine states impose estate taxes with lower thresholds—Oregon starts at $1 million. Structured settlements reduce estate values since only the present value of remaining guaranteed payments counts toward the estate, not total future payments.

Some states impose income taxes but specifically exempt structured settlement payments even when taxing other income forms. Beneficiaries should verify their state's specific treatment, though most follow federal guidelines.

Critical limitation: these tax benefits apply only to qualified structured settlements established at settlement time. You cannot create a qualified structure by taking a lump sum then purchasing a commercial annuity later—that annuity's growth would be taxable. Tax advantages require proper structuring at settlement, making the initial decision irrevocable from a tax perspective.

Tax-free compounding is the single most powerful advantage a structured settlement offers. Over twenty or thirty years, the difference between taxable investment returns and tax-free annuity payments can amount to hundreds of thousands of dollars — money that stays with the family instead of going to the government

— Robert W. Wood

Customizing Your Payout Structure: Options Beyond Monthly Payments

Structured settlements accommodate real-world financial needs through creative payment scheduling. Monthly payments provide steady income replacement, sure. But families often need more sophisticated approaches.

Balloon payments deliver larger lump sums at specific future dates. A settlement might pay $3,000 monthly with $100,000 balloons in years 5, 10, and 15—timed for a child's college enrollment, graduate school, and home purchase. These balloons come from the same annuity contract, maintaining complete tax benefits while providing flexibility for known future expenses.

Increasing payment structures address inflation. Rather than level payments forever, the annuity increases by a fixed percentage each year—commonly 2-4%. A settlement starting at $4,000 monthly with 3% annual increases reaches $6,500 monthly by year 20. Trade-off? Lower initial payments compared to level structures, since the insurance company prices in those future increases upfront.

Education funding schedules align with academic calendars. Instead of monthly checks, the structure delivers quarterly or semester-based payments during college years, then stops or converts to different amounts. A parent's wrongful death settlement for young children might include zero payments for 10 years—allowing maximum tax-free growth—then $40,000 annually for four years per child covering college, followed by lifetime income to the surviving parent.

Survivor benefits ensure money doesn't vanish if a beneficiary dies prematurely. A "10-year certain and life" structure pays for at least 10 years even if the beneficiary dies in year three—remaining payments flow to their estate. After 10 years, payments continue for life if the beneficiary survives. This protects against scenarios where a beneficiary dies shortly after settlement, leaving heirs with nothing.

Period certain versus lifetime options present a fundamental choice. Period certain annuities—10, 20, or 30 years—guarantee total payout regardless of longevity. A 30-year certain annuity pays for exactly 30 years, period. Lifetime annuities pay until death—potentially much longer than period certain, or potentially much shorter. For younger beneficiaries, lifetime structures often make sense since they might live 50+ years beyond settlement. Older beneficiaries might prefer period certain to ensure heirs receive value if they die within a few years.

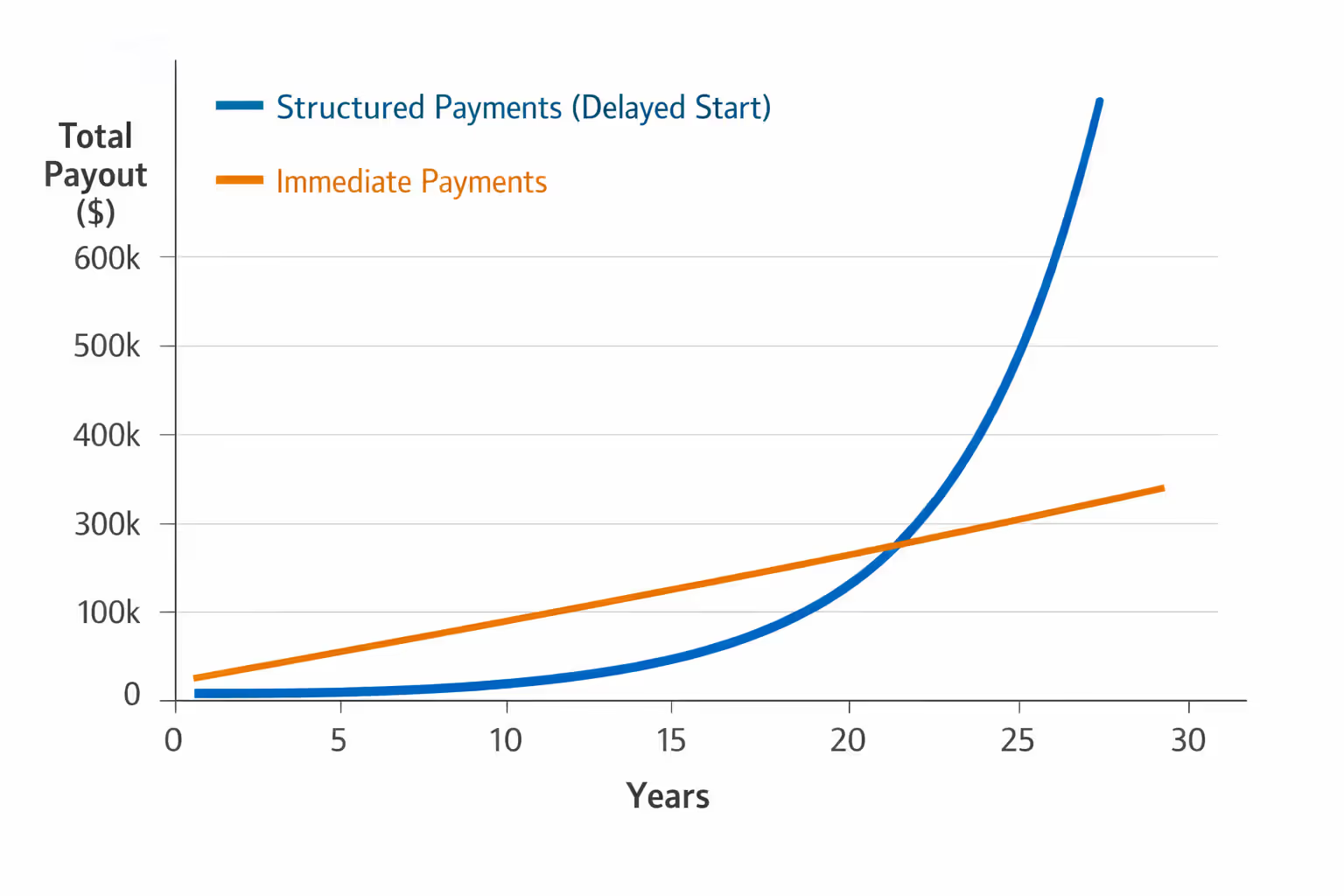

Deferred structures delay all payments to maximize growth. A minor child's settlement might defer everything until age 25, allowing 15 years of tax-free compound growth, then begin substantial monthly income. The deferral period dramatically increases total payout compared to immediate payment structures.

Author: Michael Thornton;

Source: mannawong.com

Most settlements combine multiple elements. A surviving spouse might receive $5,000 monthly for life with 3% annual increases, guaranteed minimum 20 years. The deceased's teenage daughter might receive $30,000 annually from ages 18-22 for college, then $150,000 at 25 for a home down payment, then $2,000 monthly starting at 30. These customized annuity settlement options transform a single settlement into comprehensive financial planning addressing each beneficiary's life stage needs.

Common Mistakes Families Make When Choosing Settlement Payment Plans

Underestimating longevity and future needs. A widow at 40 might live another 50 years. Structuring payments for only 20 years leaves her vulnerable in her 60s and beyond. Families obsess over immediate needs—paying off the mortgage, covering near-term expenses—without adequately planning decades ahead. Better approach? Balance immediate relief with long-term security. Perhaps take a partial lump sum for pressing debts while structuring the majority for lifetime income.

Ignoring inflation's erosive effect. Level payments of $4,000 monthly feel adequate today. In 20 years at 3% inflation? They've lost 40% of purchasing power. Families choosing structured settlements without cost-of-living adjustments must understand this trade-off consciously. The alternative—accepting lower initial payments in exchange for annual increases—feels uncomfortable when current bills loom large, but proves wise over decades.

Failing to coordinate with existing estate plans. A structured settlement might inadvertently disrupt carefully crafted estate plans. If a beneficiary's will leaves "all my assets" to specific heirs, but the structured settlement contract names different contingent beneficiaries for remaining payments? Conflicts arise. Financial planning settlements require reviewing and updating wills, trusts, and beneficiary designations ensuring all documents align.

Not considering special needs planning for disabled beneficiaries. Direct payments to a disabled beneficiary receiving Medicaid or Supplemental Security Income can disqualify them from means-tested benefits. The settlement should instead fund a special needs trust, with the trust as annuity owner and beneficiary. Payments to the trust supplement government benefits without jeopardizing eligibility. Families who structure payments directly to disabled beneficiaries often discover this mistake only when benefits terminate.

Accepting inadequate payment schedules for minor children. Courts must approve settlements for minors, but approval standards vary wildly. Some families accept structures that pay everything when the child turns 18—an age when judgment rarely matches financial responsibility. Better structures defer major payments until 25 or 30, with interim payments for education only. An 18-year-old receiving $500,000 faces enormous pressure from peers, romantic partners, and predatory "advisors."

Overlooking the impossibility of later changes. Structured settlement contracts are essentially irrevocable. While factoring companies will purchase payment rights at steep discounts (discussed below in FAQ), you cannot modify the original contract's terms. Families who later face emergencies—medical crises, business opportunities, unexpected expenses—discover they're locked into payment schedules no longer fitting their circumstances. This inflexibility demands careful upfront planning, considering multiple contingencies.

Choosing structures based on total payout rather than actual needs. Insurance companies present illustrations showing total payments over time—"$2 million settlement structured over 30 years pays $3.8 million total!" This impressive number doesn't matter if the payment schedule doesn't match when beneficiaries actually need money. A structure paying $10,000 monthly starting in 20 years might show huge total value but provides zero help with today's mortgage or tomorrow's college tuition. Long term payout plans must align with actual life events, not just maximize numerical totals on paper.

Author: Michael Thornton;

Source: mannawong.com

Working with Financial Professionals: Who Should Review Your Settlement Options

"The biggest mistake I see families make is treating wrongful death settlements purely as legal matters without involving financial and tax professionals until after terms are finalized," explains Jennifer Morrison, CFP®, a certified financial planner specializing in structured settlements at Morrison Wealth Advisors in Charlotte, North Carolina. "By the time they call me, the settlement is signed and options are locked in permanently. Proper planning requires a team approach from the very beginning—the attorney negotiates the settlement amount, absolutely, but financial planners, tax advisors, and settlement consultants should be designing the actual structure before anyone signs paperwork. I've personally seen families lose hundreds of thousands in tax benefits and financial security because they didn't involve the right professionals early enough in the process."

Settlement planning consultants specialize exclusively in structuring injury and wrongful death settlements. Unlike financial advisors who work with existing assets, settlement consultants design payment structures during active settlement negotiations. They're typically paid by the defendant's insurance company, not by plaintiffs, avoiding potential conflicts of interest. These consultants access wholesale annuity markets unavailable to retail investors, compare pricing across multiple insurance carriers, and ensure structures comply with IRS requirements for tax-free treatment. They model various payout scenarios showing total payments, tax implications, and how different structures address specific family needs.

Estate planning attorneys become essential when settlements involve minor children, disabled beneficiaries, or substantial amounts affecting estate taxes. These attorneys draft special needs trusts, coordinate settlement structures with existing estate plans, advise on beneficiary designations, and ensure settlement terms don't inadvertently create probate complications or unexpected tax problems. They also address guardianship issues for minors and incapacity planning for beneficiaries with diminished capacity.

Tax advisors or CPAs verify proposed structures maintain tax-free status, advise on state-specific tax implications, and coordinate settlements with beneficiaries' overall tax situations. They're particularly valuable for beneficiaries with existing income sources, business ownership, or complex tax circumstances. A tax advisor might identify that a beneficiary's other income pushes them into high brackets, making the tax-free nature of structured payments especially valuable. Or conversely that a beneficiary has tax loss carryforwards that could offset lump-sum investment income, reducing the relative advantage of structured payments.

Certified financial planners integrate settlements into comprehensive financial plans. They analyze how structured payments interact with retirement accounts, Social Security benefits, existing investments, and insurance coverage. CFPs help families understand whether proposed structures provide adequate income for projected expenses across multiple decades, stress-test plans against inflation and longevity risks, and coordinate settlement planning with college funding, retirement planning, and wealth transfer goals.

The ideal sequence involves assembling this team early in settlement negotiations—before accepting any settlement offer. Beneficiaries should consult with a settlement planning consultant exploring structure options, have an estate attorney review family circumstances for trust needs or estate planning considerations, and involve a financial planner ensuring the proposed structure fits within a broader financial plan.

This upfront coordination costs relatively little—often nothing out-of-pocket since settlement consultants are typically defendant-paid through the settlement process—but prevents costly mistakes that cannot be undone after settlement documents are executed.

For families navigating the devastating aftermath of wrongful death, professional guidance transforms settlement proceeds from a one-time payment into lasting financial security honoring the deceased's memory through decades of family support.

FAQ: Wrongful Death Structured Settlements Explained

Wrongful death settlements represent both tragedy and opportunity. The chance to provide surviving family members with financial stability even while grieving an irreplaceable loss.

The choice between lump sum and structured payments isn't merely financial calculation. It reflects values about security, risk tolerance, and how best to honor a loved one's legacy through practical support for those left behind.

Structured settlements excel at providing guaranteed, tax-free income streams customized to each beneficiary's needs and life stage. They eliminate investment risk, protect against mismanagement and predatory influences, and deliver inflation-adjusted income lasting decades. For many families—especially those with minor children, disabled beneficiaries, or limited financial experience—structured payments offer security lump sums simply cannot match.

Yet structures aren't universally superior in every circumstance. They sacrifice flexibility, lock families into irrevocable terms, and may underperform for sophisticated investors in certain economic environments. The right choice depends on beneficiaries' ages, financial capabilities, immediate needs, and long-term goals.

What remains non-negotiable? The need for professional guidance. Wrongful death settlements involve complex intersections of law, taxation, insurance, estate planning, and financial management. Families making these decisions while grieving deserve expert support from settlement consultants, financial planners, estate attorneys, and tax advisors who can transform settlement proceeds into lasting security.

The structure you choose today determines whether your family faces financial anxiety or stability for decades to come.