Family with two children reviewing financial settlement documents at kitchen table with laptop showing banking application

How a Wrongful Death Annuity Settlement Works Today

Content

When someone dies because another person screwed up—a negligent doctor, a distracted driver, a company that ignored safety protocols—their family faces twin nightmares. There's the grief, which never really goes away. Then there's the money problem, which shows up in every unpaid bill, every college application, every mortgage payment that suddenly has no income behind it.

You've fought through depositions, negotiations, maybe even a trial. Now you've got a settlement offer on the table. The insurance company will write you one massive check. Or they'll structure payments over time. You've got maybe two weeks to decide.

Most people have never thought about this choice before today. Yet it'll control your financial life for the next 10, 20, maybe 40 years.

Your lawyer sees it constantly—families who cash that big check, then wonder five years later where the hell all that money went. One study tracking settlement recipients found roughly 70% of people who took lump sums had burned through the money within five years. Not because they were stupid or reckless. Because managing $850,000 requires skills most folks don't have.

Annuities work differently. They convert your settlement into scheduled payments—maybe $4,200 every month for 25 years. The money arrives like clockwork. It matches how you actually spend money (monthly rent, weekly groceries) instead of dropping a fortune in your lap and hoping for the best.

What Makes Annuity Settlements Different from Lump-Sum Wrongful Death Payments

Request the full amount upfront, and you'll receive one check after the judge approves everything. Subtract lawyer fees and case expenses first. What's left hits your bank account within a few weeks.

Now it's sitting there. All of it. You're responsible for investing it, protecting it, making it last however long it needs to last.

Author: Samantha Caldwell;

Source: mannawong.com

Structured annuity compensation flips this arrangement. Your settlement money purchases an insurance contract. That insurance company promises specific payments on scheduled dates—and they're legally obligated to deliver regardless of stock market crashes, recessions, or their own investment performance.

You're essentially trading control for certainty. One lump sum? You can invest anywhere, spend on anything, save however you want. But you're also navigating those decisions completely alone. Annuities remove both the temptation and the guesswork—guaranteed income you literally cannot outlive or accidentally waste.

Types of Wrongful Death Compensation Structures

Immediate annuities kick off payments within the first year. Families who depended on the deceased's weekly paycheck need income replacement immediately—not in five years.

Deferred annuities postpone everything. Parents settling on behalf of a 10-year-old often delay payments until the child turns 18, 21, or 25. Keeps the money out of reach during potentially foolish teenage years.

Hybrid models split the settlement. Maybe you take 30% upfront to handle funeral costs, eliminate the mortgage, or pay off medical bills the deceased left behind. The other 70% becomes monthly income starting immediately.

Milestone payments create larger scheduled lump sums tied to anticipated expenses. Perhaps $45,000 arrives each September for four consecutive years to cover college costs, alongside $2,800 monthly for regular living expenses.

Who Qualifies as a Beneficiary

Your state's wrongful death statute determines who gets compensation. Surviving spouses typically come first. Children next. If neither exists, the deceased's parents might qualify. Siblings or other relatives fall further down the priority list.

Long-term partners who never married often hit legal walls. Unless you live somewhere recognizing common-law marriage or registered domestic partnerships, dating someone for 15 years grants you exactly zero settlement rights.

Financial dependency can matter more than biology. Courts might award money to a stepchild the deceased supported for a decade, even without formal adoption. Meanwhile, that 32-year-old biological son who lived across the country and never needed financial help? Probably gets nothing.

When minor children inherit money, judges must approve any settlement structure. They scrutinize these arrangements hard, making sure terms actually benefit the kid rather than making life convenient for mom's new boyfriend or grandma who wants control.

The purpose of a wrongful death settlement is not to make a family wealthy — it is to prevent a tragedy from becoming a financial catastrophe. When we structure payments for surviving spouses and children, we are building a bridge between the life they had and the life they must now navigate alone. Every decision must prioritize their long-term security over short-term convenience

— Robert J. Flemming

How Guaranteed Income Settlements Work in Wrongful Death Cases

Your settlement purchases an annuity through an insurance company that invests in government bonds, highly-rated corporate debt, and similar conservative holdings. The monthly amount you receive doesn't fluctuate with the Dow Jones or NASDAQ—it's a contractual promise backed by the insurer's reserves and your state's guaranty fund.

Once everyone signs and the court approves, you're locked in. Can't call them next year requesting different payment amounts. Can't restructure because your situation changed. This inflexibility stops you from making emotional financial decisions, but it also eliminates any adaptation if life takes an unexpected turn.

Payment Schedule Options (monthly, quarterly, annual)

Monthly distributions mirror regular paychecks. Most people budget monthly—rent due on the 1st, car payment on the 5th. Receiving $4,200 every month simplifies planning. Your $1.2 million settlement might convert to 25 years of monthly income.

Quarterly payments arrive four times annually. Some folks prefer managing larger, less-frequent deposits. Instead of twelve $4,200 deposits, you'd get four deposits of $12,600. Less administrative hassle, but you'd better know how to stretch $12,600 across three months.

Annual payments work when you're not relying on this money for daily survival. Maybe you're a widow who kept her job and doesn't need income replacement. That annual $50,000 payment in January covers property taxes, insurance premiums, and a family vacation—handled once yearly without monthly management.

Graduated payment structures increase over time. Start at $3,500 monthly with 2.5% annual bumps. Or jump from $3,500 to $5,500 monthly after 10 years when your youngest kid enters college. You're accepting lower starting payments in exchange for inflation protection or anticipated expense increases down the road.

Fixed vs. Indexed Annuity Structures

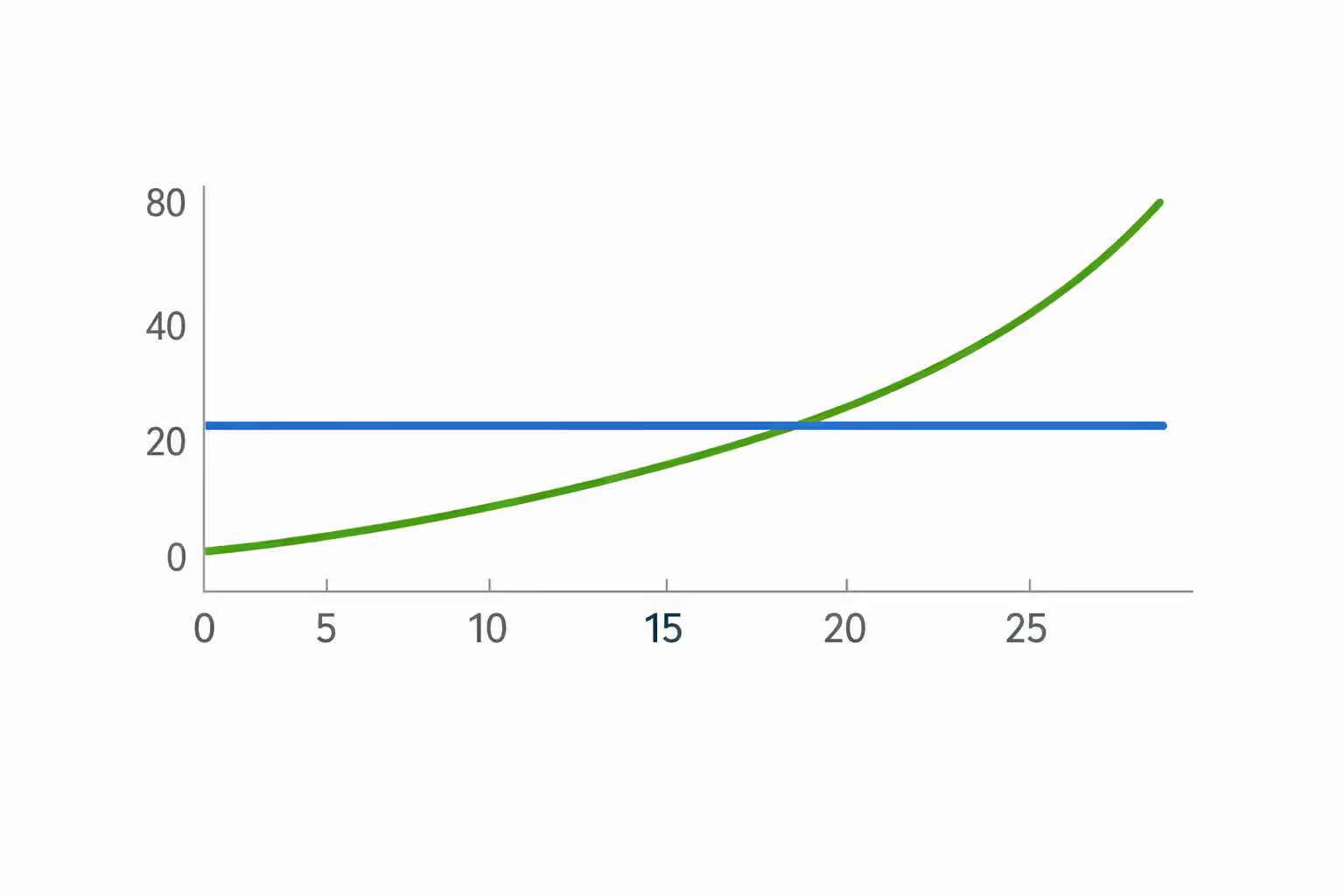

Fixed annuities deliver identical dollar amounts forever. That $4,200 monthly check never changes—same amount in year one, year 10, year 20. Perfect predictability. But inflation quietly eats away at what that money actually buys.

Indexed annuities tie payment increases to inflation measurements like CPI. When inflation hits 2.8%, next year's payments grow proportionally. You're starting with lower payments—maybe $3,800 monthly with inflation adjustments versus $4,200 fixed forever.

This trade-off becomes crucial over decades. Twenty years of steady 3% inflation cuts your purchasing power roughly in half. That $4,200 monthly payment in 2045 buys what $2,300 buys today. Indexed annuities combat this erosion, though you sacrifice immediate payment size for long-term protection.

Author: Samantha Caldwell;

Source: mannawong.com

Tax Treatment of Wrongful Death Annuity Payments: What You Need to Know

Federal tax law generally favors wrongful death settlements, though subtle distinctions create consequences families frequently miss. Understanding what qualifies as tax-free compensation versus taxable income makes a substantial difference.

| Type of Compensation | How Lump Sums Get Taxed | How Annuities Get Taxed | Tax Code Section |

| Compensation for death | Federal government doesn't tax it | Still not taxed | IRC § 104(a)(2) |

| Punitive damages (where allowed) | Taxed like wages | Same—taxed like wages | Exception to IRC § 104(a)(2) |

| Investment earnings and interest | You owe taxes each year | No taxes when structured correctly | IRC § 104(a)(2) |

| Future medical costs | Not taxable | Not taxable | IRC § 104(a)(2) |

| Lost income replacement | No federal taxes | No federal taxes | IRC § 104(a)(2) |

Here's where annuities create a major advantage: investment earnings. Take everything as one payment and invest it yourself—that $1 million might earn $40,000 annually at 4% returns. You owe income tax on those investment gains every single year.

Structured settlements eliminate that tax burden. The insurance company earns returns to fund your payments, but Section 104(a)(2) keeps your actual payments tax-free. You benefit from investment growth without annual tax bills.

Punitive damages never escape taxation, regardless of how you structure payments. Several states don't even allow punitive damages in wrongful death cases. Where they're permitted, expect ordinary income tax rates whether the money arrives as one check or multiple payments.

Most states follow federal tax treatment, though a handful impose unique rules. Always consult a tax professional who knows your specific state's approach.

Five Critical Mistakes Families Make When Structuring Settlement Payments

Underestimating Long-Term Care Costs

Healthcare costs climb faster than general inflation—sometimes doubling every decade for certain services. A 48-year-old widow might need nursing care in her seventies, when facilities run $9,000+ monthly in many areas.

Families calculate needs using today's costs: current mortgage, current grocery bills, current utilities. They ignore future medical realities. At 72, the annuity delivers $4,800 monthly while skilled nursing costs $10,000. Now what?

Smart structuring incorporates healthcare planning. Build payment increases after age 65. Schedule large payments at ages 70 and 80 specifically for medical needs. Medicare doesn't cover everything—not even close.

Author: Samantha Caldwell;

Source: mannawong.com

Failing to Account for Inflation Protection

Four thousand dollars monthly feels generous today. In two decades? Might barely cover essentials.

Annuities lacking inflation adjustments lose real purchasing power every year. The payment stays frozen while groceries, utilities, insurance, and housing costs climb. You'll still get that "generous" $4,000 check in 15 years—when it buys half as much.

Adding cost-of-living adjustments increases costs by 15-20% upfront. You might accept $3,300 monthly with inflation protection instead of $4,000 fixed. Most beneficiaries choose the higher immediate amount. Most regret it later.

Not Coordinating with Existing Estate Plans

Annuity payments to minors need guardian arrangements or trust structures. Without coordination, courts might appoint guardians you'd never choose, or payments could conflict with trusts you've carefully established.

Your beneficiary designations must align with your will and trust documents. Contradictions create legal nightmares. If your will names your sister as your kids' guardian but the annuity lists your parents as backup beneficiaries, expect problems.

Some families structure annuities while forgetting about life insurance proceeds, retirement accounts, or property the deceased owned. Total income might exceed actual needs. Or gaps appear between income sources, leaving specific years or expenses uncovered.

Ignoring Liquidity Needs

Annuities provide income, not accessible cash. When your transmission dies and repairs cost $4,500, the annuity delivers its normal $3,200 monthly schedule. It doesn't provide emergency lump sums for unexpected problems.

Keep some settlement money liquid—savings accounts, money market funds, easily accessible reserves. Many advisors suggest maintaining six to twelve months of expenses in liquid assets beyond annuity income.

Emergency car repairs, roof leaks, medical deductibles, appliance failures—life delivers unexpected costs constantly. Annuities can't flex to meet these needs. Plan accordingly.

I have seen families lose everything not because their settlement was too small, but because it lacked flexibility. A structured annuity without a liquid reserve is like a house without a foundation — it looks stable until the first storm hits. The smartest families keep six to twelve months of living expenses accessible outside their annuity, ensuring they never have to sell future payments at a devastating discount

— Dr. Patricia Navarro

Accepting Inadequate Legal Review

Settlement agreements contain language affecting your rights for decades. Beneficiaries frequently sign documents without fully understanding terms, discovering problematic provisions years later when nothing can be changed.

Courts mandate attorney representation for minors and incapacitated beneficiaries. Competent adults can technically proceed without lawyers—a dangerous economy that costs far more than attorney fees when poorly structured settlements create permanent problems.

Spend money on proper legal review upfront. You can't fix these agreements later.

Calculating Your Settlement: Factors That Determine Annuity Payout Amounts

Settlement size represents just one calculation variable. Payment duration, prevailing interest rates, beneficiary age, and structural details all impact monthly amounts significantly.

Insurance companies calculating annuity costs use mortality tables and current market rates. High interest rate environments mean your settlement purchases more monthly income. Low rates generate smaller payments from identical settlement amounts.

| Total Settlement | How Long Payments Last | Monthly Payment | Lifetime Total Received | Inflation Adjustment |

| $500,000 | 20 years | $2,900 | $696,000 | Fixed—never changes |

| $500,000 | 20 years | $2,450 | $735,000 | Increases 3% yearly |

| $1,000,000 | 25 years | $4,800 | $1,440,000 | Fixed—never changes |

| $1,000,000 | Recipient's lifetime (starts age 45) | $3,900 | Depends how long they live | Fixed—never changes |

| $2,000,000 | 30 years | $8,900 | $3,204,000 | Fixed—never changes |

| $2,000,000 | 30 years | $7,300 | $3,850,000 | Grows 2.5% annually |

These examples reflect current interest rates and standard actuarial assumptions. Your actual payments depend on when you finalize the settlement, which insurance company you choose, and your specific agreement terms.

Lifetime annuities continue until death, regardless of how long you live. Live 40 more years? You'll receive 40 years of payments. Die after five years? Payments stop unless you've purchased survivor benefits. Younger beneficiaries receive smaller monthly amounts because payments potentially continue much longer.

Period-certain annuities pay for specified terms—20 years, 30 years—whether you're alive or not. Die after 12 years of a 25-year annuity? Your estate or designated beneficiaries receive the remaining 13 years of payments.

Working with Financial Advisors: Settlement Investment Planning Steps

Wrongful death settlements demand specialized expertise. Your regular financial advisor probably lacks experience with structured settlement mechanics, tax nuances, and state-specific regulations governing wrongful death compensation.

Find professionals with relevant credentials: Certified Financial Planners specializing in settlements, attorneys practicing wrongful death and estate law, or consultants certified by the National Structured Settlements Trade Association.

Author: Samantha Caldwell;

Source: mannawong.com

Questions to Ask Before Signing Settlement Documents

What happens during genuine financial emergencies? Most structured settlements prohibit early withdrawals, though certain states permit selling future payments. You'll typically lose 30-50% of value doing this.

Can settlements fund multiple separate annuities? Absolutely, and this often makes excellent sense. One annuity handles monthly living expenses. Another funds college costs. A third provides retirement income decades from now.

What protects me if the insurance carrier fails? State guaranty associations provide coverage, typically $250,000 to $500,000 per individual per company. Larger settlements should spread across multiple highly-rated insurers to ensure full protection.

How do annuity payments interact with benefit programs like Medicaid or SSI? Payments count as income for means-tested programs. Special Needs Trusts can preserve eligibility while still providing settlement benefits.

What are the complete costs and commission structures? Structured settlement brokers typically earn commissions from insurance companies rather than from your settlement proceeds. Understand every cost involved.

Can I include death benefits for my heirs? Yes, for additional cost. You can ensure remaining payments transfer to children or other beneficiaries if you die before the annuity term ends.

State-Specific Regulations That Affect Your Options

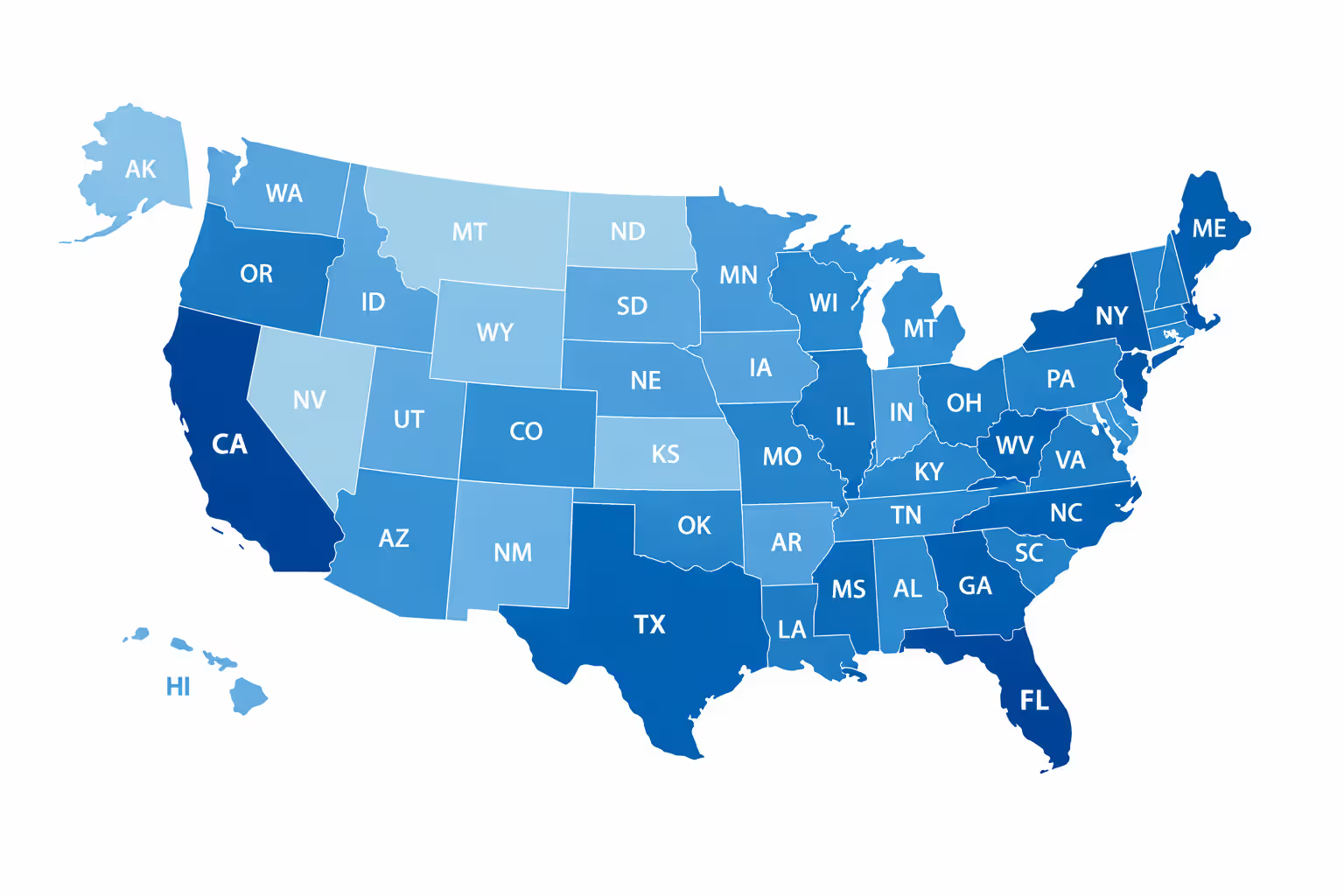

California, Florida, and New York impose particularly comprehensive structured settlement regulations. These states require judicial approval before beneficiaries can sell annuity payments later, protecting people from predatory "cash for settlements" companies.

Some states mandate specific disclosures about alternatives to lump-sum payments. Others impose waiting periods before finalizing settlement structures.

States with community property laws—Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin—handle wrongful death settlements differently depending on whether the deceased or surviving spouse receives benefits. Each applies distinct provisions.

Coverage from state guaranty associations varies considerably. Most states protect $250,000 per person per insurance company. Some provide $500,000 coverage. Specific details differ for annuities versus life insurance policies.

Workers' compensation settlements involving wrongful death operate under different rules than personal injury or negligence settlements. Several states don't even allow structuring workers' compensation death benefits as annuities.

Author: Samantha Caldwell;

Source: mannawong.com

Frequently Asked Questions About Wrongful Death Annuities

Wrongful death annuity settlements transform tragedy into lasting financial stability—when structured thoughtfully with professional guidance. These guaranteed income streams replace lost financial support, fund educational expenses, and provide household stability during grief's most challenging periods.

The permanence of these arrangements demands extraordinary care during planning. Unlike brokerage accounts where you can adjust investment strategies, annuities lock decisions in place for decades. Work with experienced professionals who understand both financial mechanics and the emotional weight these choices carry.

Start by calculating genuine needs rather than wishes. What monthly income actually maintains your household? What major expenses are approaching—college tuition, home repairs, vehicle replacement? When might healthcare needs increase substantially?

Balance immediate liquidity requirements against long-term security objectives. Hybrid approaches frequently work best: sufficient lump-sum funds for immediate expenses and emergency reserves, with remaining settlement amounts structured for predictable ongoing income.

Take inflation protection seriously, particularly for settlements lasting 20 years or longer. The purchasing power difference over extended periods justifies accepting reduced initial payments in exchange for inflation-adjusted growth.

Coordinate settlement structures carefully with existing estate plans, government benefit eligibility, and other income sources. Coverage gaps create financial stress down the road. Overlapping income sources waste precious resources.

Most importantly, resist external pressure to finalize quickly. Settlement agreements last permanently. Take necessary time to thoroughly understand available options, consult multiple qualified advisors, and ensure the structure genuinely serves your family's long-term interests. Your loved one's legacy deserves thoughtful, strategic planning that delivers security and stability for decades ahead.