Legal documents, calculator, and judge gavel on a desk representing wrongful death compensation calculation

Wrongful Death Compensation Calculator USA Guide

Content

When negligence takes someone you love, the grief hits you first. Then come the bills—medical expenses from those final hours, funeral costs, and the crushing realization that your family's financial foundation just collapsed. You're not alone in wondering what comes next financially. Thousands of families each year try to figure out what their wrongful death claim might be worth.

You've probably found those online calculators that promise to tell you what your case is worth in five minutes. They ask for your loved one's salary, punch in their age, and spit out a number. Sounds simple, right? Here's the problem: wrongful death settlements depend on dozens of factors that no computer program can properly evaluate. The state where it happened matters. Who the defendant is matters. How strong your evidence is matters. Whether your loved one left behind three kids or none matters.

In this guide, I'll walk you through what actually drives these settlement numbers—the formulas lawyers use, the traps that online calculators fall into, and when it's worth paying for real legal advice instead of trusting a website's algorithm.

What Factors Determine Wrongful Death Compensation Amounts?

Pull up any ten wrongful death settlements and you'll see everything from $40,000 to $12 million. Why such a massive spread? Because every case involves a different mix of circumstances that push values higher or lower.

Start with economic damages versus non-economic damages. Economic damages cover bills and paychecks—the financial stuff you can add up on a spreadsheet. Think about what your loved one earned, what they would've earned over the next 20 or 30 years, medical bills from their final treatment, funeral expenses. A 32-year-old architect pulling in $95,000 represents a completely different economic picture than someone who'd already retired, even if an identical accident killed them both.

Author: Daniel Whitford;

Source: mannawong.com

Non-economic damages? That's where things get fuzzy. Courts put a price on losing someone's love, guidance, and companionship. How do you quantify never seeing your spouse again? Never getting your parent's advice? The law tries, but there's no equation that feels right.

Your state's damage caps often matter more than the actual harm. California, for example, won't let you collect more than $250,000 in non-economic damages for medical malpractice deaths—period. Doesn't matter if a surgeon killed a young mother of four through obvious incompetence. The cap is the cap. Meanwhile, Pennsylvania has no cap at all for the same situation.

Comparative negligence percentages slice away at your compensation. Let's say your husband died in a crash where the other driver ran a stop sign, but your husband was speeding. The insurance company will argue he shares 30% of the blame. If the case is worth $1.2 million, you're getting $840,000 after that reduction.

Age and earning trajectory create huge valuation differences. Take two people earning $70,000 who die in similar accidents. One is 27, just finished grad school, on track for management roles and six-figure income within five years. The other is 62, planning retirement in three years. Same current salary, but decades of lost future earnings separate them.

Dependents change everything. Four kids under ten who've lost their primary breadwinner? Courts see massive financial need and profound emotional loss. An elderly parent with no dependents? Different calculation entirely. Some states actually write this into their statutes—different payout formulas depending on who survives.

The value of a wrongful death case is never just about mathematics — it’s about storytelling. The numbers lay the foundation, but what moves a jury is the human narrative: who this person was, what they meant to their family, and how their absence reshapes every single day. Calculators can add up lost wages, but they will never capture the weight of an empty chair at the dinner table.

— Thomas A. Moore

Then there's the deceased person's health before the incident. Terminal cancer patient with six months to live versus marathon runner in perfect health—obviously different life expectancy, which means different lost years to compensate. Defense attorneys will dig through every medical record to find conditions that reduce your claim's value.

Breaking Down the Damages Calculation Formula for Death Cases

Let me show you how attorneys and insurance adjusters actually calculate these numbers. It's more structured than you'd think, though still leaves room for massive disagreement.

Economic Damages: Quantifiable Financial Losses

Here's the basic formula for lost earnings:

(Yearly salary × Years to retirement) + (Projected raises and promotions) - (Money the deceased would've spent on themselves)

Author: Daniel Whitford;

Source: mannawong.com

That last part trips people up. Courts don't award the full lifetime earnings because your loved one would've used some of that money on their own needs—food, entertainment, personal expenses. For married folks, assume 25-30% gets subtracted. Single people without kids? More like 40-50%.

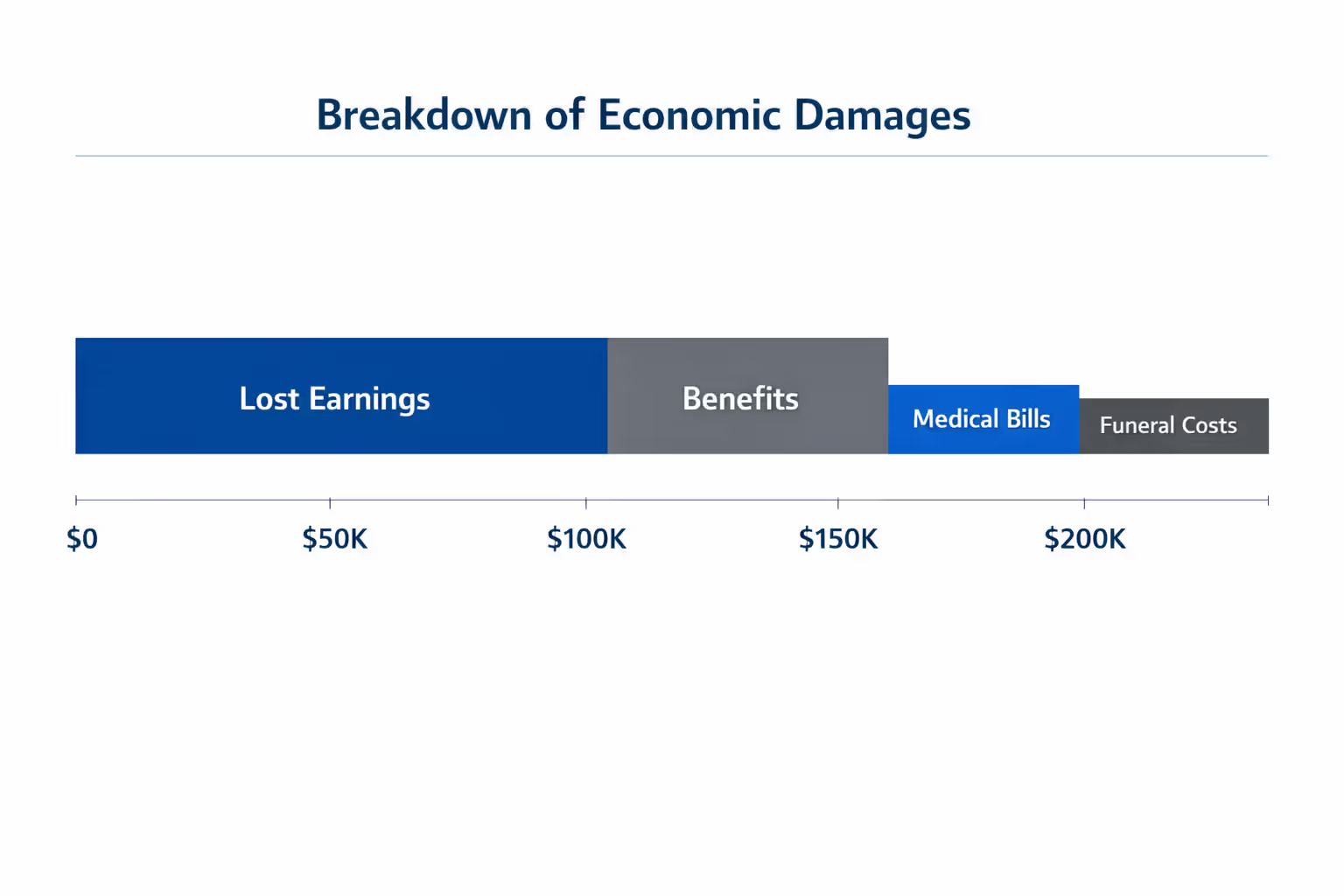

Real example: 38-year-old teacher making $65,000 with 27 years until retirement. Simple math says $1.755 million in future earnings. Add 2.5% annual raises and you're up to $2.1 million. Now subtract 28% for personal consumption—down to $1.512 million. Don't forget employer benefits: health insurance ($12,000/year), pension contributions ($5,000/year), life insurance ($800/year). Over 27 years with raises, benefits add roughly $530,000. Total economic lost earnings: $2.04 million.

But we're not done yet. Present value reduction acknowledges that money today is worth more than money in 20 years. You could invest today's settlement and earn returns. Courts apply discount rates around 2-3.5%, which typically cuts 15-25% off future earnings depending how far out they stretch. Our $2.04 million becomes roughly $1.63 million after present value adjustment.

Medical bills from the final injury add separately. Severe trauma cases rack up $200,000 to $600,000 in emergency care, surgery, ICU time, and life support before death occurs. Even a few hours in an emergency room can hit $50,000.

Funeral and burial expenses run $8,000 to $12,000 for most families. You can claim higher amounts, but courts get skeptical past $20,000 unless cultural or religious practices justify the cost.

Non-Economic Damages: Pain, Suffering, and Loss of Companionship

Here's where calculations turn into educated guesses. Two main approaches:

The multiplier method takes all economic damages and multiplies by 1.5 to 5 based on how bad the case is. Drunk driver who killed a beloved father of three in a fiery crash where he suffered for several minutes? Maybe a 4x multiplier. Distracted driver who caused instant death? Closer to 2x.

Using our teacher example with $1.63 million in economic damages, a 2.5x multiplier adds $4.075 million in non-economic damages, bringing the total claim to $5.7 million.

What pushes multipliers higher: - Defendant's conduct (intentional > reckless > negligent > simple mistake) - Pain endured before death - Young children left without a parent - Strength of family bonds - Deceased's irreplaceable role (primary caregiver, sole earner) - Jury-friendly venue

Per diem valuation assigns a daily dollar amount to loss, then multiplies by survivor life expectancy. Say a widow has 35 years of life expectancy. Value each day without her husband at $150. That's $150 × 365 × 35 = $1.916 million. This method works better for personal injury than death cases, but some attorneys use it in settlement talks.

I've practiced wrongful death law for two decades, and I can tell you that online calculators miss what actually determines case value. Two families with identical economic losses might settle for amounts $3 million apart based on how juries would perceive their loss and how badly the defendant screwed up. Any website claiming it can predict that with an algorithm is giving you fantasy numbers.

— Michael Chen, Partner, Chen & Associates Trial Lawyers, Board Certified in Civil Trial Law

State caps demolish these calculations in many jurisdictions. Remember that $5.7 million teacher case? If it's medical malpractice in California, the $4.075 million in non-economic damages gets slashed to $250,000. Total recovery: $1.88 million. Same exact death in Illinois with no cap? Full $5.7 million is in play.

How Wrongful Death Payout Estimate Tools Actually Work

These online estimators work by collecting basic information: how old was the deceased, what did they earn, how many kids, which state, what type of accident. The software runs these inputs through algorithms built from average settlements in supposedly similar cases, then displays a range.

What they ask for: - Annual income including benefits - Age when death occurred

- Number of financial dependents and their ages - Your state - Accident category (car crash, medical error, workplace incident, defective product) - Whether death was immediate or involved conscious suffering

The calculator matches your inputs to its database of past settlements, applies state-specific rules it knows about, adjusts multipliers based on accident severity, and produces an estimated range.

Why they miss the mark:

Can't evaluate whether you'll win on liability. Maybe the defendant has three witnesses saying your loved one ran a red light. No calculator knows to account for that, but it destroys your leverage in negotiations.

Don't know insurance policy limits. The at-fault driver might carry only $50,000 in coverage. Your case could theoretically be worth $800,000, but good luck collecting that from someone with no assets and minimal insurance.

Ignore litigation realities. Taking a case to trial costs $25,000 to $75,000 in expert fees, depositions, and court costs. You risk getting nothing if you lose. Settlements reflect these practical concerns—most resolve at 65-75% of theoretical full value to avoid trial uncertainty.

Can't review your actual evidence. Do you have accident scene video? Eyewitnesses? Defendant's admission of fault? Or just your word against theirs? Evidence quality moves settlement values 40-50% in either direction.

Different calculator types:

Basic multiplier versions take income times years times a fixed multiplier (usually 3x). Fastest to use, least accurate. Completely ignore your state's specific laws.

State-adjusted calculators incorporate damage caps, who can file claims, and limitation periods for specific jurisdictions. Better, but still miss case-unique factors.

Insurance company calculators use their internal settlement data. These skew low because they reflect what insurers actually pay, not what fair compensation looks like. They're designed to save the insurance company money.

Advanced estimators request details about evidence strength, defendant financial resources, and specific family dynamics. Even these can't replace an attorney who reviews your documents and knows local jury behavior.

Author: Daniel Whitford;

Source: mannawong.com

State-by-State Variations That Impact Your Lawsuit Valuation

Location determines so much about what your case is worth. An identical death with the same damages might produce a $2.8 million recovery in one state and $450,000 in another purely because of different laws.

| State | Non-Economic Damage Limits | Filing Deadline | Eligible Claimants | Punitive Awards |

| California | Medical malpractice capped at $250K | Two years from date of death | Spouse, domestic partner, children; if none exist, anyone inheriting deceased's property | Available when defendant showed malice, fraud, or oppression |

| Texas | Medical malpractice capped at $750K | Two years from date of death | Spouse, children, and parents only | Requires clear and convincing proof of gross negligence |

| Florida | Generally no caps | Two years (medical cases get four years) | Estate's personal representative filing for family | Needs clear and convincing evidence of intentional misconduct |

| New York | No caps on wrongful death damages | Two years from date of death | Estate's appointed representative only | Not available in wrongful death claims |

| Illinois | No damage limitations | Two years from date of death | Estate representative on behalf of spouse and next of kin | Allowed when willful and wanton behavior proven |

| Pennsylvania | No statutory caps | Two years from date of death | Appointed estate representative | Available for outrageous or reckless conduct |

| Ohio | Generally unlimited | Two years from date of death | Estate representative for designated beneficiaries | Requires clear and convincing evidence |

| Georgia | Medical malpractice limited to $350K | Two years from date of death | Spouse, children, parents, or estate executor | Must prove willful misconduct, malice, or fraud |

Filing deadlines are absolute. Miss your state's deadline by 24 hours and your claim is dead forever, regardless of how strong it was. A few states pause the clock while criminal prosecution is pending, but most don't.

Who can file varies significantly. Some states limit claims to immediate family. Others allow life partners, distant relatives (if no close family exists), or anyone who was financially dependent. This affects who gets paid and how courts split awards among multiple family members.

Punitive damages multiply case values in egregious situations. When defendants drove drunk, knowingly violated safety regulations, or intentionally caused harm, punitive damages punish beyond just compensating the family. States allowing punitives often see settlements 200-400% higher in extreme misconduct cases.

Different accident types trigger different rules within the same state. Louisiana treats these claims as survival actions rather than wrongful death, changing available damages completely. New Mexico caps punitive damages at either $300,000 or triple the compensatory award, whichever number is larger.

Workers' comp systems in every state provide the exclusive remedy for most workplace deaths. You generally can't sue your employer. Exceptions exist for intentional employer conduct or when a third party (equipment manufacturer, subcontractor) shares liability.

Common Mistakes When Using Compensation Prediction Tools

Families researching potential cases make predictable errors with online calculators that create false expectations and bad decisions.

Treating calculator results as guarantees causes the most problems. You see an estimate of $1.8 million and assume that's what you'll get, so you reject a reasonable $650,000 settlement offer as insulting. Calculators give you ballpark ranges, nothing more. Real outcomes depend on negotiation skill, evidence strength, and factors no algorithm captures.

Overlooking state damage caps inflates expectations dangerously. A calculator estimates $1.2 million in non-economic damages, but your state caps medical malpractice non-economic damages at $350,000. You're overestimating by $850,000. Always check whether caps apply to your specific claim type.

Forgetting about comparative fault sets you up for disappointment. Your sister died when another driver ran a stop sign, but she wasn't wearing a seatbelt. Expect the defense to argue 25% comparative negligence. Your settlement gets reduced proportionally. Most calculators never ask detailed questions about potential shared responsibility.

Author: Daniel Whitford;

Source: mannawong.com

Undervaluing non-economic loss happens when you focus only on salary. A stay-at-home mom has minimal economic damages but potentially massive non-economic value to her family. Calculators asking only about income miss this completely. Flip side: some calculators apply unrealistic multipliers that don't reflect how actual juries value these losses.

Ignoring policy limits creates the biggest gap between estimates and reality. Your case might justify $2.5 million, but the at-fault party carries $100,000 in liability coverage and owns nothing. Collecting beyond policy limits means pursuing personal assets through bankruptcy—usually recovering 10-20 cents per dollar owed.

Insurance companies have entire departments dedicated to minimizing what they pay on wrongful death claims. They know exactly which arguments reduce settlement values by thirty or forty percent. Walking into that negotiation without experienced legal counsel is like performing surgery on yourself — technically possible, but the outcome is almost always worse than having a professional do it.

— Lisa Blue Baron

Selecting the wrong case category ruins accuracy. Medical malpractice cases face different legal standards, damage caps, and typical settlements than vehicle accidents. If you classify a surgical death as a "vehicle accident" because it happened during ambulance transport, your estimate will be worthless.

Using static income figures for young professionals undervalues claims significantly. A first-year software engineer earning $85,000 has vastly different lifetime earnings than a warehouse supervisor making the same amount. Calculators that don't account for career growth miss hundreds of thousands in lost future income.

Overlooking tax consequences affects net recovery. Most wrongful death settlements avoid federal taxation, but certain components (punitive damages, pre-judgment interest) might be taxable. Calculators showing gross settlement amounts don't show what you'll actually receive after taxes and legal fees.

When to Use a Settlement Estimator vs. Hiring an Attorney

Online estimators serve a purpose early in your research, but they can't substitute for real legal evaluation. Knowing when each tool is appropriate helps you make smarter choices.

Calculators work well when:

You're just starting to research whether pursuing a claim makes financial sense. If a calculator suggests potential damages around $60,000 but litigation might cost $35,000-$45,000, that helps you assess whether the financial recovery justifies the emotional toll.

You need to understand the rough magnitude before investing time in lawyer meetings. Knowing whether you're looking at a $75,000 situation versus a $750,000 situation helps you prioritize finding representation.

You're checking whether an insurance offer is obviously terrible. An insurer offers $125,000 but even crude calculators suggest $600,000-$900,000? That's a red flag you need professional negotiation help.

You want basic talking points before discussing your case with adjusters. Understanding calculation basics prevents them from using confusing formulas to justify lowball offers.

Attorney representation becomes essential when:

Calculator estimates exceed $100,000. Cases this size justify typical attorney fees (33-40% of recovery) because skilled representation often increases your net recovery by more than the fee costs.

Author: Daniel Whitford;

Source: mannawong.com

Fault is disputed or shared between parties. When insurance companies argue your loved one bears partial blame, you need legal expertise to counter those arguments and protect your recovery.

Multiple parties share responsibility. Cases involving several defendants—maybe a drunk driver plus the bar that overserved him, or a negligent surgeon plus the hospital—require legal skill to maximize total recovery from all sources.

Medical malpractice caused the death. These cases need expert witnesses, detailed medical analysis, and specialized legal knowledge. No website adequately estimates medical malpractice values.

Your filing deadline is approaching. Most states give two years, but various circumstances can pause or extend deadlines. Attorney consultation prevents missing critical cutoffs.

The defendant lacks adequate insurance or assets. Attorneys know strategies for finding additional coverage, piercing corporate liability shields, and maximizing asset recovery.

You're facing pressure to settle immediately. Insurance companies exploit grieving families' urgent financial needs by offering fast settlements for 40-60% of fair value. Attorneys negotiate from strength rather than desperation.

Running the numbers favors attorney representation in most serious wrongful death cases. Imagine a case worth $700,000. Hiring an attorney at 35% costs $245,000 in fees, netting you $455,000. Handle it yourself and insurance companies typically offer unrepresented claimants 45-65% of fair value, knowing you lack negotiating leverage. A $350,000 offer leaves you with less than the $455,000 after attorney fees.

Attorney consultations cost nothing in initial meetings. These case evaluations provide vastly more value than online calculators. Attorneys assess evidence quality, identify liable parties you hadn't considered, explain state-specific rules affecting your situation, and give realistic settlement ranges based on actual experience with similar local cases.

Contingency fees mean zero upfront payment and nothing owed if the attorney recovers nothing. This aligns attorney incentives perfectly with yours—they maximize earnings by maximizing your recovery. It also opens quality representation to everyone regardless of current finances.

Frequently Asked Questions About Wrongful Death Compensation

Online calculators give you a rough starting point for understanding what your wrongful death claim might be worth, but they can't replace comprehensive legal evaluation of your specific situation. The most reliable assessment requires examining your actual evidence, understanding applicable state laws, identifying all insurance coverage sources, and evaluating dozens of factors that no automated tool properly analyzes.

Economic damages follow relatively predictable formulas built on lost earnings, benefits, and expenses, though even these involve nuance around career trajectories, personal consumption percentages, and present value calculations. Non-economic damages remain deeply subjective, varying dramatically based on family dynamics, defendant behavior, and jurisdiction-specific damage limitations.

State law differences often matter more than case facts—the identical death might produce a $2.8 million recovery in one state but $600,000 in another purely because of damage caps, different filing deadlines, or varying rules about who can file claims and when punitive damages apply.

Use online tools to understand basic concepts and get a sense of whether you're looking at a five-figure, six-figure, or seven-figure situation. Just recognize what they can't do: assess your evidence, negotiate with insurers, or navigate complex legal procedures to maximize recovery.

For significant claims, disputed liability situations, or complicated circumstances, professional representation typically increases your net recovery despite attorney fees. Free consultations from experienced wrongful death attorneys provide case-specific evaluations that beat any website algorithm.

Money never brings back someone you love. But fair compensation helps surviving families maintain financial stability while holding negligent parties accountable. Understanding calculation methods empowers you to make informed choices about pursuing justice after your loss.