Empty dining table with an untouched coffee cup and stack of mail envelopes in soft morning light, symbolizing absence and financial burden after loss

Wrongful Death Settlement Guide to Payouts by Case

Content

When someone dies because another person or company screwed up, the surviving family faces two separate nightmares at once. First, there's the obvious one—the unbearable emotional devastation. Second, and this catches people off guard, comes the financial crisis. Your household just lost a major income source. Bills don't stop arriving. The mortgage company doesn't care about your tragedy.

Here's what shocked me when I first started researching these cases: only about 4% actually see the inside of a courtroom. Why? Insurance companies hate juries. They can't control what twelve random people might decide. A sympathetic jury could award three times what the company budgeted. Meanwhile, families can't afford to wait 36 months for a trial verdict while maxing out credit cards and draining college funds.

So both sides usually negotiate. The tricky part? Figuring out whether that offer on the table actually reflects your loss, or if it's just the first lowball number they throw at everyone hoping you'll bite.

What Determines the Value of a Wrongful Death Settlement?

Every attorney you consult will probably dodge your "what's my case worth?" question with something vague. It's not because they're being cagey—these calculations genuinely depend on dozens of moving pieces. A software engineer making $140,000 who dies at 33 creates a completely different financial picture than a retired teacher killed at age 78, even though both deaths matter equally in human terms.

Economic Damages in Death Cases

Start with damages you can actually measure. Insurance adjusters love this section because it involves spreadsheets instead of emotions.

Lost income and workplace benefits create the biggest numbers in most claims. Picture a 40-year-old dentist earning $185,000 yearly with potentially 27 working years ahead. The salary alone—ignoring promotions or raises—hits $4.995 million. Forensic accountants dig deeper, though. They factor in likely salary increases based on industry trends, retirement contributions the employer would've matched, health insurance worth perhaps $18,000 annually, and continuing education stipends. These economists pull data from the Bureau of Labor Statistics and examine the person's actual work history to project realistic career growth.

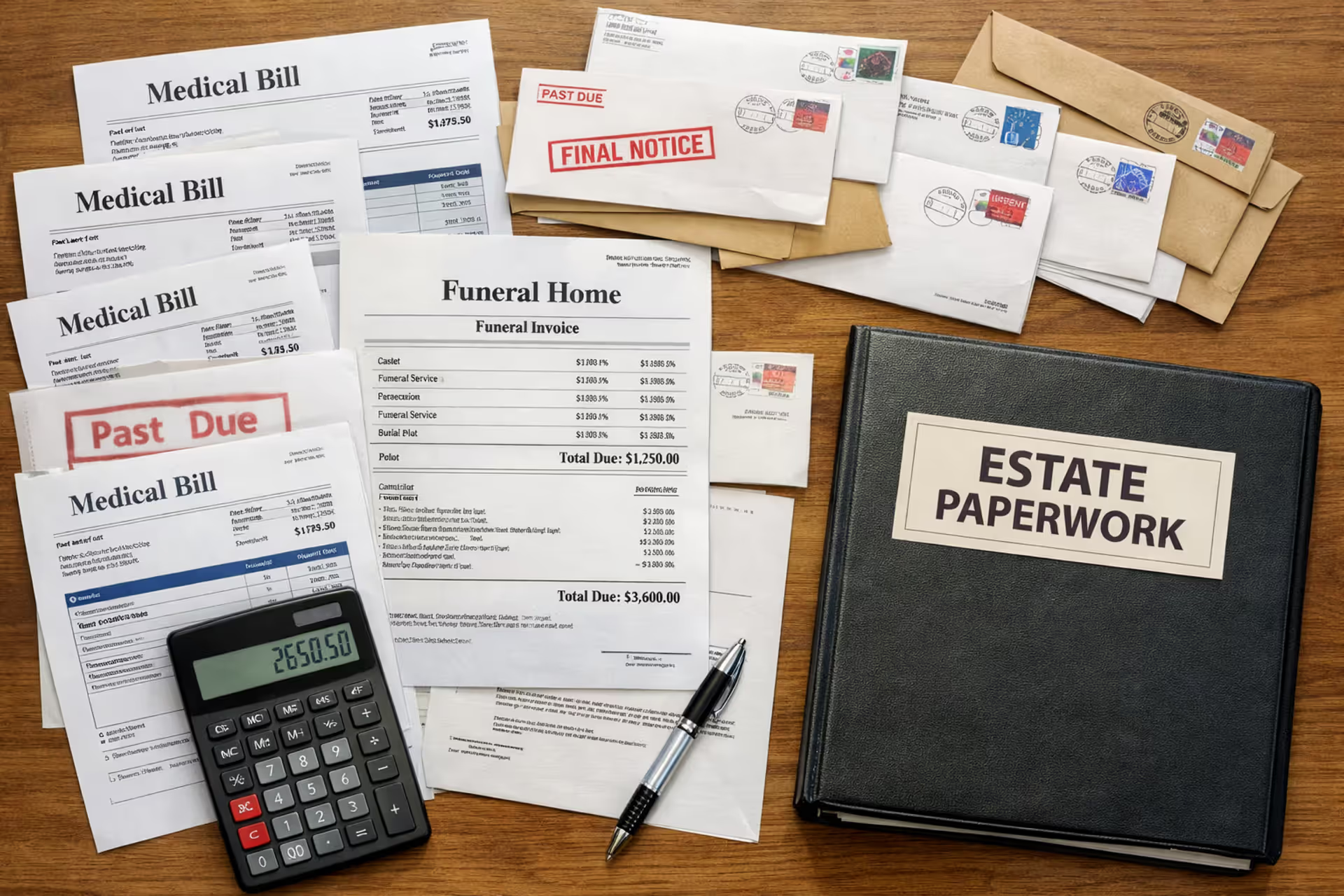

Medical costs before death get included whether the person survived three hours or three weeks. Someone who spent four days in intensive care before dying might generate $180,000 in hospital bills. Emergency helicopter transport, multiple surgeries that ultimately couldn't save them, specialist consultations, medications—every medical expense tied to the fatal injuries counts.

Burial and funeral costs slam families immediately, usually landing between $7,000 and $15,000. In expensive metro areas, cemetery plots alone can run $8,000. These expenses hit right when families are emotionally wrecked and least equipped to handle financial decisions or scrape together cash.

Lost household services get routinely ignored, especially when the deceased wasn't bringing home a paycheck. Think about a stay-at-home parent managing three kids—coordinating schedules, cooking meals, shuttling everyone to activities, cleaning, tutoring homework. That work has measurable economic value. Replacing it means hiring childcare providers, housecleaners, tutors, and drivers. Conservative estimates put replacement costs at $55,000 to $75,000 per year.

Author: Samantha Caldwell;

Source: mannawong.com

Non-Economic Damages and Pain and Suffering

Here's where the spreadsheet becomes useless. You can't build a formula that captures what your mom's advice meant. There's no calculation for the hole left when your spouse doesn't come home anymore.

Loss of companionship and relationship tries to address the permanent absence from survivors' lives. Someone who lost a husband of 32 years lost their retirement travel partner, the person they discussed everything with, their closest friend. Parents whose 19-year-old daughter died lost her future wedding, grandchildren they'll never meet, decades of shared holidays. The quality of the relationship weighs more heavily than simple duration. A close, mutually dependent relationship differs fundamentally from a distant or strained one.

Psychological damage and emotional trauma varies dramatically between survivors. Some develop major depression requiring ongoing medication and therapy. Others develop PTSD—panic attacks when triggered by certain sights or sounds, chronic anxiety, intrusive memories that won't stop. One person might need eight months of counseling. Another might require psychiatric treatment indefinitely. Courts increasingly recognize these individual differences deserve separate consideration.

Lost parental guidance and nurturing hits children especially hard. An 8-year-old whose father died won't have him present for middle school challenges, high school decisions, college applications, first heartbreak, first job, or their own wedding someday. That kid won't get their dad's advice on handling bullies, choosing friends, or navigating adult responsibilities. Recent court decisions increasingly attach substantial value to these losses beyond pure economics.

The deceased person's age, health status, and life expectancy dramatically change these calculations. A healthy 36-year-old might have shared 50 more years with their family. An 85-year-old with congestive heart failure had shorter life expectancy—though their life absolutely mattered and their loss creates genuine suffering.

The law cannot restore life to the dead, but it can ensure that those left behind are not destroyed twice — first by grief and then by financial ruin. The measure of a just legal system is how it protects the most vulnerable in their darkest hour.

— Morris Dees

Punitive Damages in Wrongful Death Claims

This category exists purely to punish. It's not about making families whole—compensatory damages handle that job. Punitive damages tell defendants: "What you did was so reckless we're imposing extra financial pain to make sure you never do it again."

Think about a trucking company that deliberately violated federal safety regulations, forced drivers to work 16-hour shifts despite legal limits, and skipped required brake inspections to save money. When their exhausted driver with faulty brakes causes a fatal crash, punitive damages make sense. Or consider a medical device manufacturer that buried internal research showing their product caused strokes, then kept selling it anyway. That's punitive territory.

The problem? Regular negligence doesn't qualify. Defendants must have acted with "willful and wanton disregard for safety" or something similar depending on your state's standard. Someone who glanced at their phone and caused a fatal accident probably won't face punitive damages. That same person on their sixth DUI? Now we're talking.

State laws throw up major roadblocks around these damages. Many cap them at two or three times compensatory awards. Some require "clear and convincing evidence"—a higher standard than normal civil cases use. Several states ban punitive damages in wrongful death cases entirely, regardless of how outrageous the conduct.

How Wrongful Death Settlement Amounts Are Calculated

Insurance adjusters and plaintiff's lawyers approach valuations from opposite directions, but they reference similar frameworks. Understanding their thinking helps you spot an insulting offer versus genuine negotiation.

Multiplier methods dominate personal injury practice. Take economic damages—let's say $650,000—and multiply by something between 1.5 and 5 depending on case strength. A case with crystal-clear liability, devastating loss, and sympathetic facts might justify multiplying by 4.5. A case where fault looks murky and damages seem modest might only warrant 1.8. This isn't scientific, but it gives both sides a starting framework.

Per diem calculations try assigning daily monetary values to ongoing suffering. An attorney might argue each day without the deceased costs $300 in lost companionship. For someone age 42 with 38 years of life expectancy remaining, multiply $300 by 13,870 days to get $4.16 million. Many judges now reject this approach as too speculative, though some lawyers still argue it.

Jury verdict databases provide reality checks. Experienced attorneys track what actually happens in comparable cases within their jurisdiction. They know that medical malpractice death cases in their county typically settle between $900,000 and $2.5 million, while car accident deaths average $350,000 to $1.4 million. These historical patterns shape expectations dramatically.

| Case Type | Typical Settlement Range | Key Factors Affecting Amount |

| Medical malpractice | $500,000 – $3,000,000+ | Whether the medical error was obvious; deceased person's age and income; whether your state caps damages |

| Motor vehicle accidents | $250,000 – $2,000,000+ | How clear the fault evidence looks; available insurance limits; deceased person's income and family situation |

| Workplace deaths | $500,000 – $2,500,000+ | Whether workers' comp applies; whether other companies share liability; whether safety violations were documented |

| Nursing home negligence | $300,000 – $1,500,000 | Evidence of systematic abuse patterns; state inspection violations; deceased person's health before the negligence |

| Product liability | $750,000 – $5,000,000+ | Whether the manufacturer knew about the danger; whether other injuries followed similar patterns; whether punitive damages apply |

These numbers reflect negotiated agreements, not jury awards. Trial outcomes swing much more wildly based on jury composition, witness performance, lawyer skill, and factors nobody can predict.

Insurance policy limits create frustrating ceilings no matter what your actual losses are. Imagine a drunk driver carrying only $100,000 in coverage who kills a software developer earning $165,000 annually. That family legitimately lost millions in future financial support. But if the drunk driver only has $100,000 coverage and owns no meaningful assets, that's your ceiling unless you can find additional defendants—maybe the bar that kept serving him after he was visibly drunk.

Author: Samantha Caldwell;

Source: mannawong.com

The Settlement Negotiation Process: Step-by-Step Timeline

Negotiations follow predictable patterns, though individual circumstances add complications that stretch or compress timelines.

Initial Demand Letter and Response

Your lawyer will typically spend four to seven months collecting documentation before sending formal demands. This letter lays out everything: what happened, why the defendant is responsible, what your family lost, and what you're demanding as compensation.

Lawyers deliberately inflate these demands to preserve negotiating space. Your attorney might genuinely believe the case is worth $1.2 million but demand $2.1 million. This accomplishes two goals: it anchors negotiations higher, and it creates room for "compromise" that still hits the actual target.

Insurance adjusters usually respond within 30-60 days with offers that feel offensive. On that $2.1 million demand, they might counter $350,000. This is standard theater—don't freak out. Both sides understand they'll eventually land somewhere between these numbers. The adjuster who immediately offered $1.5 million would get fired for failing to protect company money. Your lawyer who accepted $350,000 without pushing back would be committing malpractice.

Discovery and Evidence Exchange

When initial talks stall, attorneys file lawsuits to access formal discovery tools. Depositions force witnesses to answer questions under oath. Document requests uncover internal emails and records. Expert witnesses prepare detailed analyses. Each piece shifts negotiating leverage.

Discovery frequently uncovers surprises that dramatically change settlement positions. Maybe a deposition catches the defendant contradicting their earlier police statement. Perhaps their medical expert witness comes across as unqualified or unconvincing. On the flip side, discovery might reveal the deceased had undisclosed prior health conditions affecting life expectancy calculations. Each new revelation changes the power dynamic.

Industry secret: settlements spike dramatically after discovery wraps but before serious trial prep begins. At this point, both sides know enough to realistically assess their chances without having dumped massive money into trial preparation they'd prefer avoiding.

Mediation vs. Going to Trial

Most courts now require mediation before allowing trials. A neutral mediator—often a retired judge—manages negotiations. Parties stay in separate rooms while the mediator shuttles back and forth carrying offers, counteroffers, and reality checks.

Mediation resolves roughly 75% of remaining cases because the structured environment removes some emotional barriers. A skilled mediator tells your side, "Look, juries in this county tend conservative on death cases. Your $1.8 million expectation might become $700,000 at trial." Then they tell the defense, "Your offer is insulting. They'll take this to trial on principle alone, and you could end up paying $2.5 million." That neutral pressure breaks deadlocks.

Families who reject settlement and push toward trial are gambling, period. Juries might award substantially more than settlement offers—sometimes triple. Or they might deliver verdicts so low they don't even cover your attorney's advanced costs. Trials also delay payment by eight months to two years through appeals.

According to attorney David Ball's published research on damage awards: "Handing your case to twelve strangers and asking them to value your loss is inherently unpredictable. They don't know your family, they didn't experience your loss, and they're being asked to translate grief into dollars—something humans aren't equipped to do consistently."

Author: Samantha Caldwell;

Source: mannawong.com

Common Mistakes That Reduce Your Settlement Amount

Families navigating these claims frequently sabotage their cases through understandable but costly mistakes.

Accepting the first offer rarely makes financial sense. Insurance companies structure initial offers expecting they'll negotiate upward. They're counting on overwhelmed, grief-stricken families being too exhausted to fight. A family accepting $225,000 immediately might have eventually gotten $575,000 with proper representation and patience. Initial offers typically represent 25-45% of ultimate settlement values.

Social media activity destroys cases constantly. That beach vacation photo posted six months after your wife's death? Defense attorneys will blow it up poster-size and argue you're clearly not devastated. Privacy settings offer zero protection—discovery requests pierce them easily. The only safe approach is complete social media silence during active litigation.

Missing statutory deadlines kills otherwise strong cases instantly. Statutes of limitations typically give families one to three years from the death date to file lawsuits. Miss that deadline—even by 24 hours—and your case vanishes regardless of its merits. Courts show absolutely zero mercy on these time limits. They're rigid and inflexible.

Talking directly to insurance adjusters creates ammunition used against you. Insurance companies call grieving survivors pretending they want to help while recording everything. They'll ask innocent-sounding questions like "How are you managing?" If you say "We're doing okay," they'll later argue your suffering isn't severe. Everything gets twisted to minimize their payment.

Inadequate documentation of losses makes proving damages unnecessarily hard. Save every receipt for therapy sessions. Document all missed work. Keep prescription records for anti-anxiety medication. Track every financial impact. Years later when settlement talks begin, these records prove invaluable.

Hiring the wrong lawyer might be the most expensive mistake possible. Wrongful death litigation demands specialized knowledge. Your buddy who handles real estate deals or your cousin who drafts wills won't have the expertise to maximize your settlement. Attorneys who regularly handle these specific cases understand valuation strategies, negotiation tactics, and litigation approaches that can double or triple outcomes compared to inexperienced representation.

In my experience, grieving families lose more money through preventable mistakes than through any fault in the legal system itself. Silence, patience, and expert counsel are not luxuries — they are the three pillars that separate a fair outcome from a devastating one.

— Thomas A. Mauet

Timeline for Receiving Your Wrongful Death Settlement

Timeline questions lack universal answers, but recognizable patterns emerge.

Straightforward cases with obvious liability sometimes resolve within 10-16 months. Think about a pedestrian killed by someone texting while running a red light. Liability looks clear, damages are documented, insurance exists—negotiations move relatively quickly when basic facts aren't disputed.

Complex cases with disputed liability easily stretch to 28-48 months or longer. Medical malpractice claims require multiple expert reviews. Product defect cases involve technical engineering analysis. Each complexity layer adds months.

After signing settlement agreements, payment typically arrives within 30-60 days in most jurisdictions. The defendant or their insurer sends a check to your attorney's trust account. Your lawyer deducts their contingency fee, reimburses case costs they advanced, resolves any liens, and distributes remaining money according to state law.

Structured settlements spread compensation across years or decades instead of one lump sum. You might get $125,000 immediately, then $3,800 monthly for 15 years, totaling $809,000.

Various factors create delays nobody controls. Court schedules in major cities might set trial dates 20 months out. Defendants sometimes file bankruptcy, freezing everything until bankruptcy proceedings finish. Cases with multiple defendants turn into finger-pointing contests where each tries shifting blame to others, complicating settlement considerably.

Understanding Your Settlement Agreement: What You're Actually Signing

Settlement documents contain legally binding terms permanently affecting your family's rights. Understanding what you're agreeing to prevents ugly surprises later.

Release of liability forms form the core of every settlement. You're promising never to sue the defendant again for anything connected to this death. Once you sign and cash the check, it's over—permanently. You can't come back later after discovering new information or realizing the settlement fell short. This finality is absolute and irreversible.

Pay attention to how broadly releases extend. Settling with a negligent driver might simultaneously release their employer, the car manufacturer, the bar that served them, and the insurance carrier. Make certain you understand precisely which parties you're releasing, particularly when multiple potential defendants exist.

Confidentiality clauses appear in many agreements. Defendants pay premiums—sometimes $50,000 to $125,000 extra—for provisions preventing families from publicly discussing settlement amounts. Some add broader restrictions preventing any case discussion whatsoever.

These raise ethical questions worth serious consideration. Should your family accept bonus money to stay silent when speaking out might protect others? A nursing home buying your silence might continue abusing residents. A manufacturer paying for confidentiality keeps selling dangerous products. Only your family can weigh immediate financial needs against potential public benefit from transparency.

Lump sum versus structured settlements involves significant trade-offs worth careful analysis. Taking everything now gives maximum flexibility. Pay off your mortgage, fund education accounts, invest however you choose. Structured arrangements guarantee long-term income and protect against poor money management but lock funds away from immediate access.

Tax treatment differs substantially between these options. Wrongful death proceeds themselves generally avoid federal income tax, but interest earned on structured payments faces taxation. Investment gains from lump sums also create tax liability. Consulting a tax professional before choosing payment structure prevents expensive mistakes.

Government reimbursement claims sometimes consume substantial settlement portions. If your loved one received Medicare or Medicaid before death, federal law grants the government reimbursement rights from your settlement. These liens can eat $25,000, $45,000, or more from settlement proceeds, reducing what actually reaches your family. Attorneys experienced in wrongful death know strategies for negotiating these liens downward, but can't always eliminate them entirely.

Author: Samantha Caldwell;

Source: mannawong.com

Frequently Asked Questions About Wrongful Death Settlements

Reaching settlement closes one difficult chapter while opening another. The financial resources provide important security, but they don't erase the empty chair at dinner or the voice you'll never hear again.

Many families benefit from working with financial advisors specializing in managing substantial settlements. Sudden wealth creates unique challenges, particularly for people grieving and making decisions under emotional stress. Professional guidance helps ensure settlement funds serve their intended purpose: long-term security and honoring your loved one's memory through wise financial stewardship.

Estate planning becomes critical after receiving substantial compensation. Update your will to reflect these new assets. Consider establishing trusts for minor children that protect funds until they mature enough to manage them responsibly. Plan for tax-efficient wealth transfer to protect settlement proceeds from being depleted by estate taxes or creditor problems.

Grief counseling and support groups help families process loss beyond the legal mechanics. The settlement process often delays emotional healing because families focus on litigation rather than grief work. Once the case concludes, addressing grief directly becomes both possible and necessary.

The legal system's approach to wrongful death remains imperfect. No settlement check brings someone back or repairs the damage done. But these mechanisms serve important purposes: they provide financial stability when families desperately need it, force negligent parties to face consequences for their actions, and acknowledge that your loss genuinely matters. Understanding how settlements actually work gives families the knowledge to navigate this difficult process and secure compensation that reflects what they've truly lost.