Person reviewing bills and wrongful death claim documents at a table.

Wrongful Death Lawsuit Funding Guide for Families

Content

When someone you love dies because another person acted negligently, you're drowning in grief while bills pile up fast. The funeral home wants $10,000 by Friday. Your mortgage payment is due, but the paycheck that always covered it stopped coming. Medical bills from those final hospital days fill your mailbox. Meanwhile, your attorney explains that your wrongful death case will probably take eighteen months—maybe three years—to settle.

That's where wrongful death lawsuit funding enters the picture. These cash advances let you tap into your expected settlement money right now, today, instead of waiting years while your case works through the legal system.

But here's the thing: this money costs a lot. Sometimes a shocking amount. Before you sign anything, you need to understand exactly how these advances work, what you'll actually pay, and whether the steep price makes sense for your situation.

What Is Wrongful Death Lawsuit Funding?

Think of this funding as selling a piece of your future settlement at a discount to get cash immediately. Companies in this business—often called pre-settlement funders—give you money now based on what they think your wrongful death claim will eventually be worth. You get cash today. They collect later when your case settles.

Here's what makes this different from the car loan or mortgage you're used to: if your case loses, you don't owe a penny. Nothing. This "non-recourse" setup means the funding company only gets paid if your lawsuit wins or settles. They're gambling on your case. If the gamble fails, they eat the loss completely.

The process works like this: the funder examines your lawsuit, estimates what it's worth, then offers you maybe 10% or 15% of that amount upfront. So if they think your case will settle for $400,000, they might offer you $40,000 now. When your case eventually settles, they'll take back that $40,000 plus their fees—which could easily total $60,000 or $80,000 depending on how long everything takes.

Who actually gets approved? You need an active wrongful death lawsuit already filed in court with a lawyer representing you. You can't get funding on a claim you're just thinking about filing. Your attorney has to cooperate with the funding company too, since they'll need detailed case information and will get repaid directly from the settlement check.

The big difference from regular loans: Bank loan officers care about your credit score, your job, your income—basically, whether you can pay them back from your paycheck. These legal funders couldn't care less about any of that. They're evaluating your lawsuit, not your finances. Someone with an 800 credit score and a six-figure salary gets rejected if their case looks weak. Someone who's broke and has terrible credit gets approved if their wrongful death claim looks rock-solid.

Why do advance funding death claims cost so much more than borrowing from a bank? Because the funding company might lose everything. Banks get their money back no matter what happens to you—they'll garnish wages, seize assets, wreck your credit. Funding companies have exactly one way to get paid: your case has to win. That massive risk is why they charge massive fees.

Author: Daniel Whitford;

Source: mannawong.com

How Pre-Settlement Funding Works for Death Claims

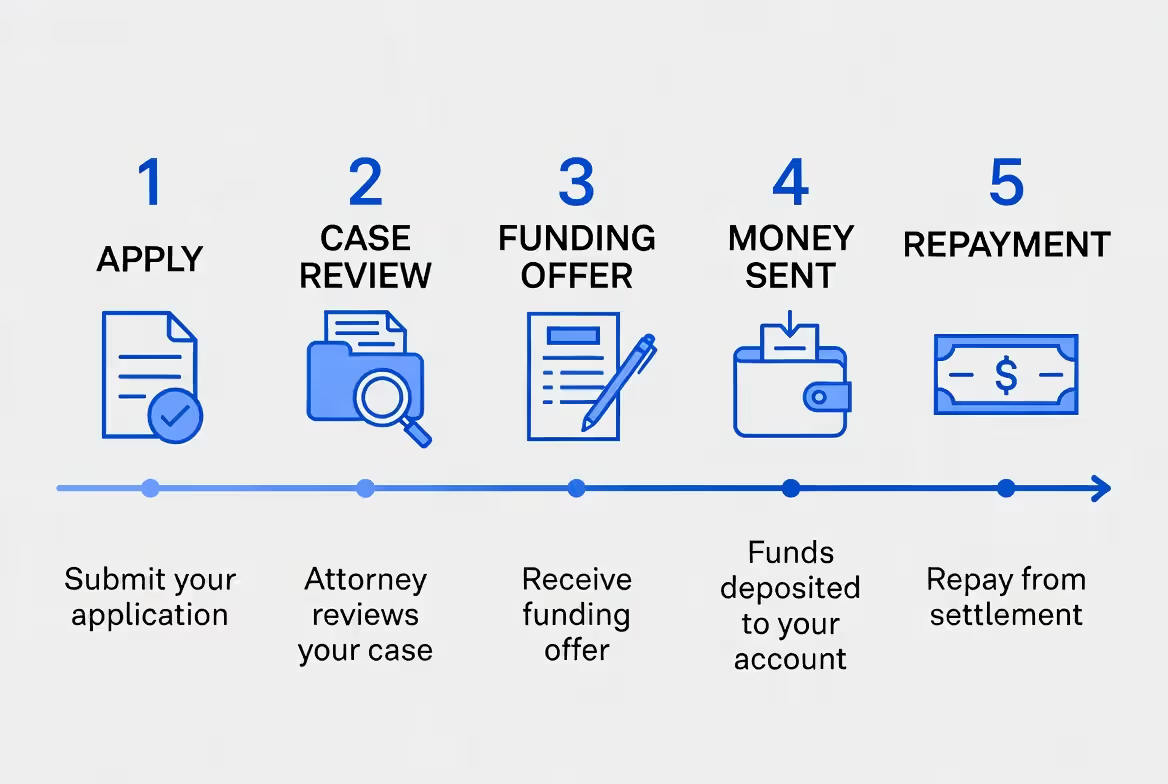

Getting funded typically takes one to three days. When families need money urgently, some companies can move even faster. Here's how it unfolds:

Step one—you apply: Call or fill out an online form with basic information. Your name, your lawyer's name and phone number, a quick description of how your family member died and who you're suing. How much money you need right now. You'll sign a form letting the funder talk to your attorney about the case details.

Step two—they investigate your case: The company contacts your lawyer and requests documentation. They want to see the lawsuit complaint you filed, any evidence collected so far, expert witness reports if you have them, information about the defendant's insurance coverage, and details about settlement discussions if any have happened. They're trying to answer three questions: Is liability clear? Are the damages substantial? Can the defendant actually pay a judgment?

Step three—you get their offer: If they like what they see, you'll receive a funding contract. Read every word carefully, or better yet, have your attorney read it. This document spells out the advance amount, the fee structure, and the repayment calculation. Some funders charge a flat percentage regardless of timing. Others use monthly rates that compound, meaning your cost grows every single month your case drags on.

Step four—money hits your account: Sign the agreement and funds typically arrive within a day, sometimes within hours. Check, wire transfer, or direct deposit into your bank account. Nobody monitors how you spend it—use it for the funeral, the mortgage, groceries, medical bills, whatever you need.

Step five—repayment happens automatically: Your case eventually settles (or you win at trial). Your attorney receives the settlement check, pays the funding company their portion directly from those proceeds, takes their own fee, pays any case expenses, then sends you what's left. If you lose your case instead, you keep the advance money and walk away. The funder loses their investment entirely.

Real example: A family lost their father in a truck accident. Applied for pre settlement funding legal advances on a Monday afternoon. Their attorney sent case files to the funding company Tuesday morning. By Wednesday noon they had a $30,000 offer in hand. Thursday the money was in their checking account. Their case settled fourteen months later for $725,000. The funding company took $47,500 (the original $30,000 plus $17,500 in accumulated fees). After the attorney's contingency fee, the family netted about $437,000.

Types of Litigation Financing Options Available

Author: Daniel Whitford;

Source: mannawong.com

You've got several paths to access money while waiting for your settlement. Each works differently and costs differently.

Lawsuit Loans vs. Settlement Cash Advances

People use these terms like they mean the same thing, and for practical purposes they basically do. But there's a technical distinction worth understanding.

Lawsuit loans explained: Despite what the name suggests, you're not actually borrowing money in the traditional sense. There's no loan that you must repay regardless of what happens. Instead, you're selling a chunk of your future settlement rights. The "lender" is actually buying a piece of your claim. If your wrongful death lawsuit tanks and you recover zero dollars, you owe zero dollars back. Traditional loans don't work that way—banks want their money back whether you got hit by lightning or won the lottery.

Settlement cash advances: This term more accurately describes the transaction. You're getting tomorrow's money today. The funding company pays you present dollars in exchange for future settlement dollars, keeping the difference as their profit. The gap between what they give you and what you pay back—that's how they make money. And if your case takes forever, that gap gets wider and wider.

Why the naming matters: Some states regulate these products as loans, which brings certain consumer protection laws into play. Other states treat them as investments or asset purchases, which might mean different regulations or none at all. From where you're sitting though, the result is the same—immediate cash in your pocket in exchange for a bigger chunk out of your settlement later.

Attorney-Based Funding Arrangements

Sometimes your lawyer can help with funding directly, which usually costs less than going to outside companies:

Attorney liens explained: Your lawyer advances you money from their own pocket against the fee they'll eventually earn from your case. Say they're working for a 33% contingency fee and they advance you $8,000. When your case settles, they deduct that $8,000 (maybe with modest interest) from their share of the fee. This typically costs way less than commercial funding because attorneys charge lower rates and they've already got skin in the game—they want your case to succeed.

Law firm credit facilities: Bigger firms sometimes set up lines of credit specifically for client advances. They can offer reasonable interest rates because they've got capital and they understand the case intimately. These arrangements still require repayment from the settlement, but the terms beat commercial funders.

The catch: Most attorneys, especially solo practitioners or small firms, simply can't afford to loan clients money. They're already working on contingency, meaning they don't get paid unless the case wins. Fronting additional cash on top of that free work? Many lawyers just can't swing it financially. Even firms willing to help might cap advances at a few thousand dollars—not nearly enough when you're facing $50,000 in immediate needs after a wrongful death.

Regular personal loans: Banks and online lenders will loan you money based on your credit and income. Interest rates run anywhere from 6% to 36% APR depending on your financial profile. You have to pay the money back whether your lawsuit succeeds or fails. But if you can qualify for one, the total cost over time will be dramatically lower than lawsuit funding—we're talking tens of thousands of dollars in savings on a large advance.

Home equity loans: If you own a house with equity in it, you can borrow against that value at rates around 7% to 10% in 2026. There's risk—if you can't repay, you could lose your home. But for cases with strong odds of settling, the cost savings compared to lawsuit funding can easily exceed $50,000 on a substantial wrongful death claim.

Author: Daniel Whitford;

Source: mannawong.com

Costs and Risks of Legal Funding Companies

Legal funding companies charge more than any bank, credit union, or credit card you've ever encountered. Way more. They're taking enormous risk—they only get paid if your case wins—so they charge accordingly.

Monthly compounding rates: Most funders charge between 2.5% and 4.5% per month, compounding monthly. Let's break down what that actually means. You take a $20,000 advance at 3% monthly. After twelve months, you owe $27,680. After two years? $38,280. Three years? $52,960. You borrowed twenty grand and you're paying back nearly fifty-three grand. That $20,000 cost you almost $33,000 extra—you paid 165% of what you borrowed.

Flat fee structures: Some companies keep it simpler. They charge a set percentage added to your advance no matter how long the case takes. For instance, a 40% fee means your $20,000 advance requires $28,000 repayment whether you settle in eight months or four years. You get cost certainty this way, and it helps you if your litigation drags on forever.

Hybrid pricing models: A handful of funders mix approaches—maybe 2% monthly for the first year, then it switches to a flat 25% fee after that. Always calculate what you'd owe under different timelines. What if your case settles in six months? One year? Three years? Run all the scenarios.

What happens when you lose your case: You keep every dollar they gave you. The funding company loses their entire investment. This protection is exactly why the pricing feels so extreme—funders need to profit enough on winning cases to cover their losses on losing cases, plus make money overall.

How these fees eat your settlement: Picture this. Your wrongful death case settles for $500,000. Sounds like a lot, right? You took a $50,000 advance at 3% monthly and your case took eighteen months to settle. You now owe $85,750 to the funding company. Your attorney takes their 33% contingency fee, which is $165,000. After the funder gets paid ($85,750) and your lawyer gets paid ($165,000), you're left with $249,250. That's less than half the gross settlement. Without that funding advance, you would've taken home $335,000.

Lawsuit funding fills a real need for families in genuine financial emergencies, but it should be your absolute last option after you've exhausted everything else. I've seen effective annual rates exceed 40%, sometimes climbing past 100% for cases that stretch across several years. Families need to actually do the math and seriously consider whether they can bridge the gap through family help, credit cards, or just cutting expenses rather than giving up such a huge portion of their recovery.

— Margaret Chen

One danger nobody talks about enough: settlement cash advance risks include pressure to settle too early. As those funding fees pile up month after month, plaintiffs start feeling desperate to accept whatever settlement offer is on the table, even if it's way below what the case is truly worth. Your case might be worth $800,000 if you go to trial, but the defendant offers $500,000 to settle early. If you've already racked up $100,000 in funding obligations, accepting that lower offer starts looking necessary even though waiting would ultimately net you more money after paying back the advance.

When Wrongful Death Lawsuit Funding Makes Sense

Despite the eye-watering costs, certain situations genuinely justify advance funding death claims:

You're about to lose your house: Foreclosure proceedings are moving forward and you're three weeks from eviction. You've got no other options. Taking a lawsuit advance prevents you from becoming homeless. Yes, it costs a fortune, but compare that cost to the long-term devastation of foreclosure and homelessness.

Funeral and burial bills are due now: Death-related expenses typically run $8,000 to $12,000, and funeral homes want payment immediately. Most families don't have that kind of cash sitting around. Credit cards or personal loans cost less if you can get them, but lawsuit funding provides an option when you can't access traditional credit.

Your household income vanished overnight: The person who died was earning most or all of the family income. The paychecks stopped but the bills didn't. Wrongful death settlements compensate for those lost future earnings, but that money might be years away. Funding bridges the gap so you can keep the lights on and feed your kids while the lawyers do their work.

Your case will definitely take years: Complex wrongful death claims—medical malpractice, defective product cases, situations where fault is disputed—often stretch across 2-4 years or even longer. You can't put your entire life on hold that long. Strategic use of advances, taking only what's absolutely critical, helps you survive extended waiting periods.

Having money gives you negotiating leverage: This seems backwards, but it's true. Defense lawyers know which plaintiffs are desperate. Desperate people accept lowball offers because they need money NOW. When you're not financially desperate because you've already covered your urgent needs, you can reject those inadequate offers and wait for fair value. Sometimes the funding cost gets offset by a higher final settlement.

Other options you should try first:

- Borrow from family members (put it in writing with clear repayment terms to protect the relationship)

- Contact a credit counselor to set up debt management plans that reduce your monthly bills

- Call your creditors directly, explain you've got a pending settlement, and negotiate payment plans or temporary forbearance

- Apply for temporary government assistance—food stamps, Medicaid, housing assistance, utility assistance

- Sell things you don't absolutely need or downsize to cheaper housing

- Pick up part-time work or gig economy jobs if you're physically and emotionally able

Here's a useful guideline: Can you survive without funding by tightening your belt and using cheaper forms of credit? Then do that. Will not getting funding result in you being homeless, starving, or facing some other genuine crisis? Then the cost might be justified. Don't use lawsuit advances for discretionary spending—every dollar you take costs you two or three dollars from your settlement.

How to Choose a Reputable Legal Funding Company

Author: Daniel Whitford;

Source: mannawong.com

The litigation financing industry includes both ethical companies and absolute predators who exploit desperate plaintiffs. Protect yourself:

Clear disclosure of all costs: Legitimate legal funding companies explain their fees in plain English, in writing. They tell you whether rates are monthly or annual, whether they compound, and what you'd owe if your case settles in six months versus two years. Run from companies that only tell you the advance amount without explaining what you'll pay back.

Proper state licensing: More and more states now regulate lawsuit funding, requiring companies to get licensed, capping their fees, and mandating disclosure standards. Verify that the company you're considering complies with your state's laws. Unlicensed operators can charge illegal rates and use aggressive tactics.

Your attorney's opinion matters: Your lawyer should know the funding company or at least be willing to check them out. If your attorney specifically warns you away from a particular funder, listen to that advice. Lawyers work with these companies repeatedly and they know which ones create problems.

Contract terms requiring close attention:

- Caps on maximum repayment (better companies limit total repayment to 2-3 times the advance)

- Requirements about communicating with your attorney (they should inform your lawyer about all interactions)

- The specific settlement rights you're assigning (make sure language limits it to just the advance amount)

- Hidden fees (application fees, processing charges, or other costs beyond the stated rate)

Red flags screaming "predatory funder":

- Pushing you to sign immediately without letting your attorney review it

- Vague or deliberately confusing explanations of their fees

- Asking you to communicate behind your attorney's back

- Encouraging you to take more money than you actually requested

- No physical address listed or no state licensing information available

- Rates so extreme that the effective APR exceeds 100%—shop around because some funders charge way less

Questions you absolutely must ask before signing:

- If my case settles in six months, what's the exact dollar amount I'll owe? What about twelve months? Twenty-four months?

- Are there any fees whatsoever beyond the interest or flat fee you've disclosed?

- Can I repay early if I want to, and are there prepayment penalties?

- How does it work if I need additional money later in the case?

- Do you have a license in my state, and are you following all state regulations?

- Can I take this contract home and spend two days reviewing it with my attorney before I sign?

Shop around. Seriously. Rates and terms vary wildly among legal funding companies. Getting quotes from three different companies can save you tens of thousands of dollars on a large wrongful death advance.

| Funding Type | Credit Check Required | Repayment if Case Lost | Approval Time | Typical Fees |

| Pre-settlement funding | No | You keep the money | 24-48 hours | 25%-100%+ of the original advance |

| Personal loan | Yes | You must repay regardless | 1-7 days | 6%-36% annual percentage rate |

| Credit card cash advance | Minimal | You must repay regardless | Immediate | 25%-30% APR plus 3%-5% upfront fee |

| Home equity loan | Yes | You must repay regardless | 2-6 weeks | 7%-10% annual percentage rate |

Frequently Asked Questions About Wrongful Death Lawsuit Funding

Wrongful death lawsuit funding delivers immediate financial relief while you're waiting months or years for your settlement, but you'll pay a steep price for that relief. Families facing genuine emergencies—imminent foreclosure, inability to pay for a funeral, complete loss of household income—might need advances despite the expense. The non-recourse structure protects you if your case loses, but successful cases surrender a substantial chunk of the recovery to funding fees.

Before you pursue lawsuit funding, exhaust every cheaper alternative first: borrow from family, negotiate payment plans with your creditors, cut your expenses to the bone, or tap traditional credit if you can qualify. If you genuinely need an advance, take only the minimum amount absolutely necessary. Get quotes from several funding companies. Review the contract carefully with your attorney. Make sure you understand exactly what you'll pay back under different settlement timelines.

The right funding company gives you transparent terms, complies with state regulations, and works cooperatively with your attorney. The wrong company traps you in exploitative terms that devour half your settlement. Choose carefully, calculate the true cost, and use lawsuit funding as the genuine last-resort financial tool it should be—not a convenient way to get settlement money early, but a lifeline when literally no other options exist.